The moment you hear the words "slab leak," your mind probably jumps straight to the cost. It’s the big question on every homeowner's mind: will my insurance policy actually cover this?

The honest answer is a bit complicated. Generally, your standard homeowners policy may step in to cover the water damage caused by a sudden leak, but it almost certainly won't pay to fix the broken pipe itself.

What Your Homeowners Insurance Actually Covers

It helps to think of your insurance policy as a safety net for sudden, unexpected accidents. When it comes to slab leaks, that "sudden and accidental" distinction is everything. A pipe that spontaneously bursts is a classic example of an accident. On the other hand, a pipe that's been slowly dripping for months because of rust is often seen as a maintenance problem you were expected to handle.

Most policies draw a hard line between two parts of a slab leak disaster:

- The Aftermath: This is the damage the water causes once it escapes the pipe—think warped hardwood floors, drenched drywall, ruined carpets, and damaged furniture. Your policy will most likely cover these repairs.

- The Source: This is the actual failed pipe buried beneath your concrete slab. The cost to access and repair that specific piece of plumbing is almost always excluded.

It All Comes Down to the "Why"

The reason for the leak is the most critical piece of the puzzle. If the pipe failed because of a "covered peril"—an event your policy specifically lists as being covered—you’re in a good position to have the resulting damage paid for. Think of a sudden, catastrophic burst.

But if the leak is the result of a slow, gradual issue like old age, rust, or shoddy work from a previous plumber, your claim could be denied. Insurance companies operate on the principle that homeowners are responsible for regular upkeep. An old, corroded pipe that finally gives out is usually viewed as a maintenance failure, not a true accident.

The rule of thumb for slab leak coverage is this: Policies are built to cover the effect (the water damage) of a sudden accident, not to fix the cause (the faulty pipe) or pay for problems that developed slowly over time.

To make this clearer, here’s a quick breakdown of what’s often covered versus what’s not when dealing with a slab leak.

Quick Guide to Potential Slab Leak Coverage

| Damage Component | Often Covered | Often Excluded |

|---|---|---|

| Water Damage | Repairing soaked drywall, flooring, and cabinets. | N/A |

| Personal Property | Replacing damaged furniture, rugs, and electronics. | Items damaged by a slow, long-term leak. |

| Pipe Repair | N/A | The cost to fix or replace the actual broken pipe. |

| Tear-Out & Access | The cost to break through the slab to reach the pipe. | The cost to find a leak without a clear origin. |

| Mold Remediation | If it's a direct result of the covered water damage. | Mold from a slow leak or poor maintenance. |

| Gradual Damage | N/A | Damage from wear and tear, rust, or corrosion. |

This table is just a guide, of course. Your specific policy language is what ultimately matters, but it illustrates the general approach most insurers take.

The Financial Stakes for Homeowners

Slab leaks are a major source of water damage claims across the country, and the costs can be staggering. While the national average to repair just the leak itself is around $2,300, the average insurance claim for the resulting water damage often tops $12,500. That number shows just how fast the collateral damage adds up.

For more on how insurance generally handles plumbing failures, check out our guide on homeowners insurance for busted pipes. You can also get a broader perspective by reading this excellent article on whether Is Water Damage Covered by Homeowners Insurance.

Understanding What Your Homeowners Policy May Cover

When you discover a slab leak, one of your first panicked thoughts is probably, "Am I covered for this?" It’s a fair question, because insurance policies can be incredibly confusing. So let's talk about what that policy actually means in the real world.

The answer almost always hinges on one key phrase: "covered peril." This is insurance-speak for a specific, sudden, and accidental event your policy agrees to pay for. Think of a pipe bursting under your home because of a sudden spike in city water pressure—that’s a classic example. It’s an accident, not the result of a slow, predictable decay you could have prevented.

When that kind of unexpected event happens, two parts of your policy typically come into play to help you recover.

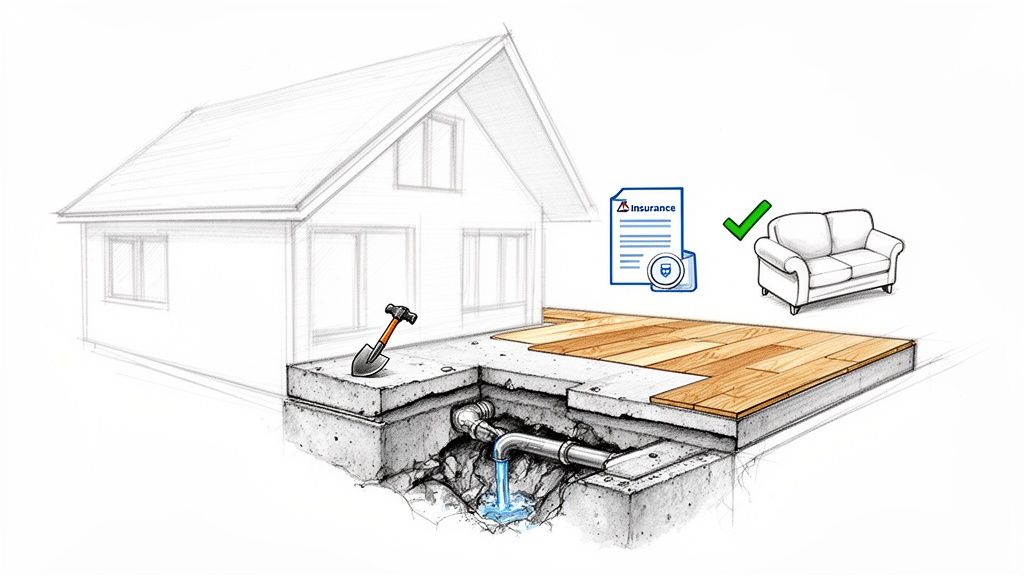

Dwelling Coverage for Access and Repairs

Your policy's dwelling coverage (often called Coverage A) is there to protect the physical structure of your house. When a slab leak is caused by a covered peril, this is the part of your policy that can be a lifesaver, covering some of the most expensive and destructive parts of the repair.

Getting to a leaking pipe under a concrete slab is no small feat. It involves messy, heavy-duty work that dwelling coverage often helps pay for:

- Tear-Out and Access: The cost to physically break open your concrete foundation to get to the broken pipe. This is a major job, and many policies may cover it if it’s necessary to fix the water damage.

- Structural Repair: After the plumber finishes, you’re left with a giant hole in your foundation. Dwelling coverage helps pay to patch the concrete and put your home back together, ensuring its structural integrity.

- Resulting Water Damage: This is the visible mess you see—the soaked drywall, warped flooring, and ruined baseboards. Dwelling coverage is designed to cover the cost of repairing or replacing these parts of your home damaged by the water.

In short, the policy often pays for the demolition needed to get to the leak and the reconstruction needed to put your home back together. What it almost never covers is the cost of the new pipe itself.

When a slab leak is caused by a sudden, covered event, your policy isn't just about the water damage. It may also cover the considerable expense of accessing the leak by breaking the slab and then repairing that slab after the plumbing is fixed.

Slab leak coverage often comes down to the cause being a 'covered peril' instead of wear-and-tear. Policies like the HO-3 Special Form usually provide the broadest protection. With these policies, a sudden pipe burst can trigger dwelling coverage for both the slab repair and the water damage restoration, which can average $5,000 per job. While your personal items might be covered, the actual pipe repair or rerouting—costing an additional $4,000-$10,000—is typically your responsibility. You can read a detailed guide about slab leak repair for a deeper dive.

Personal Property Coverage for Your Belongings

A slab leak doesn't just damage your house; it can destroy your stuff. This is where your personal property coverage (Coverage C) becomes crucial.

If water from a covered leak soaks your living room, this is the coverage that helps you replace your ruined couch, soggy rugs, and fried electronics. The rule is the same as for your home's structure: the damage has to come from a sudden, accidental event.

So, if that burst pipe leads to a warped antique dresser that can't be saved, Coverage C is what you’ll use to help cover the loss. It’s the part of your policy that protects the things that make your house feel like home.

What Insurance Typically Won't Cover With a Slab Leak

While having a good homeowners policy can be a huge relief when disaster strikes, it's just as important to know what isn't covered. Honestly, this is where most of the surprises and frustrations happen for homeowners. When it comes to slab leaks, you need to go in with your eyes open about these common policy limits.

The number one reason a slab leak claim gets denied is gradual damage. It's a simple concept, but it trips up a lot of people. Insurance is built for the "sudden and accidental"—a pipe that bursts unexpectedly. It’s not designed to cover problems that have been slowly developing for weeks, months, or even years.

A tiny, persistent drip from a rusty pipe that you never knew existed? That's a classic example of what an insurer will likely call a maintenance issue, not a covered catastrophe.

The "Gradual Damage" Sticking Point

Think of your plumbing like the tires on your car. You're expected to maintain them, check the pressure, and eventually replace them when they get old and worn. Your insurance company looks at your home's pipes the same way. They expect you, the homeowner, to handle basic upkeep.

When a pipe finally gives out because of a slow-moving problem, the insurer often sees it as a predictable failure, not a random accident.

Here are the usual culprits that fall under this exclusion:

- Wear and Tear: Nothing lasts forever, especially the pipes hidden in your foundation. A leak caused by rust, corrosion, or simple old age is almost always on you, not the insurance company.

- Deferred Maintenance: Did you notice your water bill creeping up? Or maybe see a small damp spot you decided to "keep an eye on"? If there were warning signs that were ignored, an insurer will likely deny the claim for the major damage that follows.

- Improper Installation: If the leak happened because a plumber did a shoddy job years ago, that's often considered a construction defect. Your insurance company will argue it's not a covered accident.

This is a really critical distinction. Even if the final event feels like a sudden flood, if the investigation shows the root cause was long-term corrosion, the whole claim could be denied. This gray area is where countless homeowner-insurer disputes begin.

The Pipe Itself Is Almost Never Covered

This one catches nearly everyone by surprise. Even if your policy agrees to cover the water damage, it will almost certainly not pay to repair or replace the actual broken pipe.

The cost of buying and installing the new plumbing section is viewed as a home maintenance expense. Your policy is there to fix the damage the water caused to your home, not to upgrade your plumbing system itself.

So, let's say it costs $3,000 to jackhammer the concrete slab and then repair the flooring. Your insurance may cover that. But the $500 the plumber charges to actually replace that piece of faulty pipe? That will probably come straight out of your pocket. It's a small but important cost to be prepared for.

Other Big Exclusions to Watch Out For

Beyond gradual damage, a few other standard exclusions can immediately shut down a slab leak claim. You need to be aware of them.

- Earth Movement: If the ground shifts or your foundation settles, cracking a pipe in the process, that damage is typically excluded. You'd need a separate, specialized earthquake policy for that.

- Flooding: This term has a very specific meaning in insurance. "Flooding" is when water comes into your home from the outside (like from a storm or overflowing river). It has nothing to do with a pipe bursting inside your house and requires a completely separate flood insurance policy.

- Groundwater Seepage: This is a tricky one. If a pipe breaks under the slab and the water soaks the ground before seeping back up through the concrete, some adjusters might try to call it a "groundwater" issue and deny the claim.

- Mold from Neglect: Your policy might cover mold that grows as a direct result of a sudden, covered leak (though often with strict limits). But if the mold is from a slow, ignored leak, you're on your own. It’s a complicated topic, and you can learn more about whether homeowners insurance covers mold to understand the fine print.

How To Navigate The Insurance Claim Process

Finding out you have a slab leak is one of the most gut-wrenching moments a homeowner can face. The stress is immediate. But filing the insurance claim doesn't have to be another source of anxiety. Knowing what to do—and in what order—can make all the difference in getting your home and life back to normal.

Think of this as your playbook for the moment you first suspect a problem.

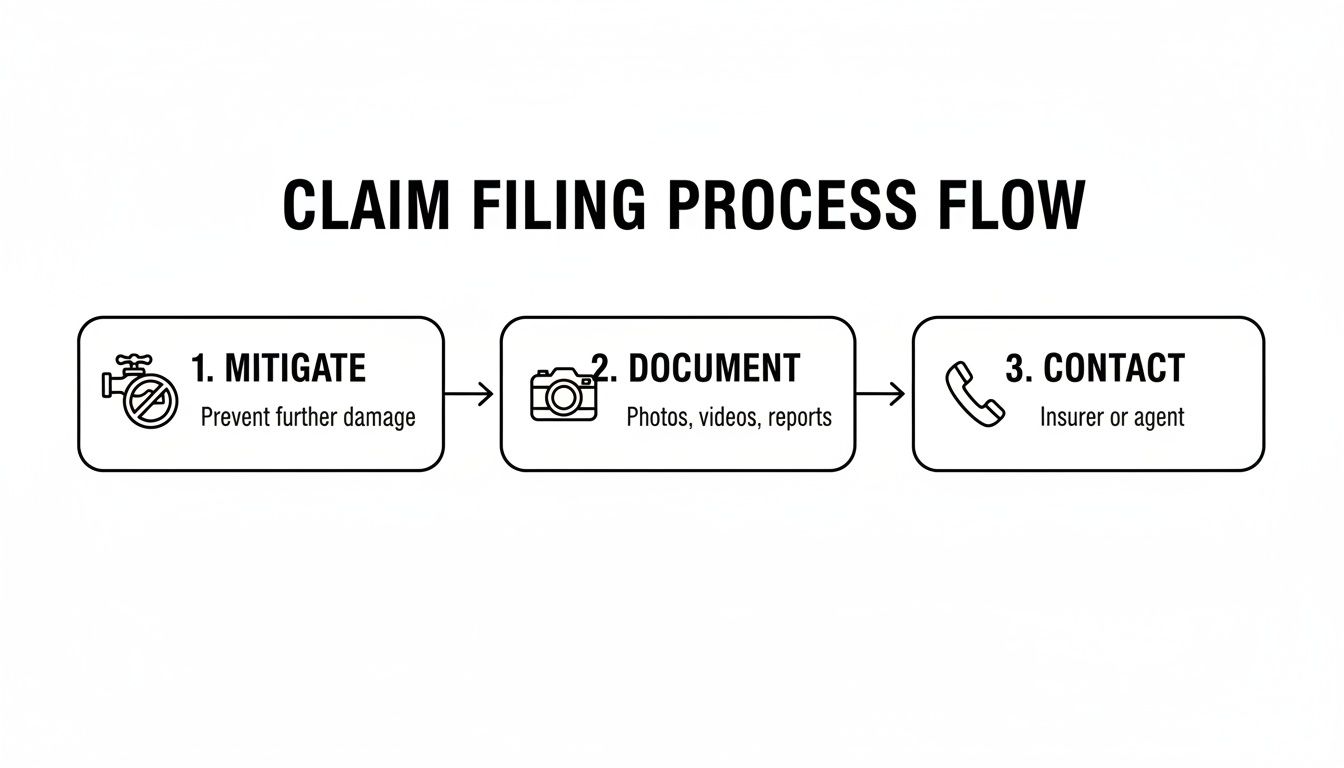

Your absolute first priority is to stop more damage from happening. This isn't just good advice; it's a condition of your insurance policy. The moment you see water, find your home’s main water supply and shut it off. Then, your next call should be to a professional restoration company. Every minute counts.

Document Everything Before Anyone Touches A Thing

Before the cleanup crew arrives, it's time to put on your detective hat. Grab your phone and start taking photos and videos of everything. Get shots from different angles, capturing the standing water, the soaked drywall, the warped flooring, and any furniture or belongings that have been damaged.

The more visual evidence you have, the stronger your claim will be. Once you've done your own documentation, find your insurance policy and call your agent to get the claim started. You’ll need to tell them the date you discovered the water.

The reality is, the burden of proof is on you. This is why professional documentation from a certified restoration firm is so powerful. Their moisture meters, thermal cameras, and detailed drying logs give the insurance adjuster the objective, third-party data they need to approve a claim without a fight.

Understanding The Key Players

Once you file your claim, you’ll start dealing with a couple of key people. Knowing who does what is crucial for keeping the process smooth.

- The Insurance Adjuster: This person is employed by your insurance company. Their job is to investigate what happened, look at the damage, and figure out how much the insurance company may pay based on the fine print in your policy.

- Your Restoration Contractor: This is your expert in the trenches. A company like Restore Heroes works for you. We’re here to stop the damage, make the repairs, and build the rock-solid documentation needed to support your claim.

A good restoration team will handle the back-and-forth with the insurance company, submitting the detailed reports, photos, and estimates they require. This frees you up to focus on your family while the experts manage the paperwork and negotiations. And for more insider advice, check out our water damage insurance claim tips.

The Reality Of Filing A Claim

Filing a claim for a slab leak is often a necessity, but it helps to go in with your eyes open. While a sudden and accidental pipe burst may be covered, denials are common. Insurers may argue the leak was due to "wear and tear," which can leave 25-35% of homeowners stuck with the entire bill.

Success often comes down to proving the leak was an unexpected event, not a slow, predictable failure. In fact, poor documentation is a leading cause of claim failure, contributing to as many as 20% of denials.

Consider this: In the Southwest, the average slab leak claim was $18,000. Homeowners who brought in a professional restoration company right away saw their claim approval rates jump by as much as 40%. Why? Because of the professional photos, moisture maps, and drying logs that left no room for doubt. You can learn more about these insurance claim findings on ConsumerAffairs.com to get a clearer picture.

Your Step-by-Step Claim Checklist

When you’re dealing with a slab leak, everything happens fast. Having a checklist can help you stay organized and ensure you don’t miss a critical step that could impact your claim.

Here’s a simple guide to follow from the moment you discover water.

Slab Leak Claim Filing Checklist

| Step | Action Item | Why It's Important |

|---|---|---|

| 1. Mitigate Damage | Shut off the main water valve immediately. | Prevents further water damage and shows the insurer you took responsible action to limit the loss. |

| 2. Call Professionals | Contact a 24/7 restoration company like Restore Heroes. | Their team can start drying out the structure, which is crucial for preventing secondary damage like mold. |

| 3. Document | Take extensive photos and videos of all visible damage before anything is moved. | This visual evidence is your primary proof for the adjuster, showing the initial extent of your loss. |

| 4. Contact Insurer | Call your insurance agent to report the claim and get a claim number. | This officially starts the process and gets an adjuster assigned to your case so things can move forward. |

| 5. Get an Assessment | Have the restoration company provide a detailed damage report with moisture readings. | Professional, data-driven reports are more credible and help justify the scope of work needed for repairs. |

| 6. Meet the Adjuster | Be present when the insurance adjuster inspects the property. Your contractor should be there too. | Allows you and your expert to walk them through the damage, point out hidden issues, and ensure nothing is overlooked. |

| 7. Keep Records | Save every receipt, report, and email in a dedicated folder. | A clear paper trail is essential for tracking expenses, managing the process, and resolving any potential disputes later on. |

Following these steps provides a clear, documented path from disaster to restoration, giving your claim the best possible chance for a smooth and successful outcome.

The Financial Side of a Slab Leak Claim

Let's talk about the money side of things. Even if your insurance claim for a slab leak is approved, it’s not a completely free ride. You need to get a handle on the real costs—both what you'll pay now and what it could mean for your budget later—to decide if filing a claim is your best move.

First up is your deductible. Think of this as your buy-in. It's the amount you have to pay out of pocket before your insurance company chips in a single dollar.

For example, if your policy has a $1,000 deductible and the total covered damage comes out to $10,000, you’ll pay that first $1,000. Your insurer then picks up the remaining $9,000. The deductible you choose plays a big part in your premium; a higher deductible usually means a lower monthly payment, and vice-versa.

Breaking Down What You’ll Actually Pay

Beyond your deductible, other costs will almost certainly pop up. Remember how we said insurance covers the damage from the water, not the pipe itself? That means the plumber's bill to fix the actual leaky pipe is typically on you, even while insurance pays for tearing out the concrete and putting your floors back together.

This is where you have to make a smart financial call. If the total repair cost is just a bit over your deductible, filing a claim might not be worth the hassle. Let's say you have a $2,500 deductible and the total covered damage is $3,000. You'd only get $500 from the insurance company, which might not be enough to justify a claim on your record.

The real kicker? Filing a water damage claim can cause your insurance premium to go up at renewal time. Insurers often see a water claim as a red flag for future risk, and your rates might reflect that.

This chart lays out the very first steps you need to take. It all boils down to stopping the damage, documenting everything, and then making the call.

As you can see, what you do in those first few moments—like shutting off the water and snapping photos—sets the foundation for your entire claim.

To File or Not to File? Weighing Your Options

Deciding whether to file a claim is more than a simple math problem. You have to look at the bigger picture.

Here are the main things to consider:

- The Scale of the Damage: If you’re looking at catastrophic damage that will cost tens of thousands to fix, that's exactly what insurance is for. Don't hesitate to use it.

- Your Deductible vs. the Cost: Get a solid repair estimate and compare it to your deductible. If the numbers are close, paying out of pocket could save you from a rate hike down the road.

- Your Recent Claim History: Have you filed any other claims in the last few years? Insurers get nervous about multiple claims in a short timeframe, and it could even lead them to not renew your policy.

Trying to estimate the true cost can feel like guesswork. That’s why we put together a guide to give you a clearer idea of how much water damage repair costs. Making an informed choice is the best way to protect both your home and your wallet.

Why Your First Call Should Be to a Restoration Pro

When you find water seeping up from your floors, your first instinct might be to call a plumber or a general cleanup crew. But in the case of a slab leak, that can be a big mistake. What you really need is a certified restoration professional—someone who acts as your advocate and understands the ins and outs of slab leak insurance coverage.

Here’s something most homeowners don't realize: your insurance policy has a "duty to mitigate" clause. This simply means you’re required to prevent the problem from getting worse. A restoration company with a 24/7 emergency response team helps you do just that. They don’t just clean up; they stop the damage cold, which is the first step to a successful claim.

The Difference Professional Certification Makes

Anyone can set up a few fans, but only a certified technician understands the science of drying out a home. This is where credentials from the IICRC (Institute of Inspection, Cleaning and Restoration Certification) aren't just a nice-to-have; they’re critical for your insurance claim.

IICRC-certified pros follow a strict, scientific method. They don’t guess. They measure.

- Total Water Extraction: They use powerful equipment to pull standing water out of your floors and walls before it can cause permanent damage.

- Scientific Drying: Using moisture meters, they map out the wet areas and strategically place industrial-grade air movers and dehumidifiers to dry everything properly.

- Mold Prevention: Their goal isn't just to make things look dry. It's to get them scientifically dry, preventing a hidden mold problem from cropping up weeks later.

This professional approach does more than just save your house. It creates a bulletproof paper trail of photos, moisture readings, and reports that prove to your insurance company exactly what needed to be done.

A great restoration company is your translator. They speak the same language as the insurance adjuster, providing the precise documentation needed to get your claim approved without a fight.

Having an Experienced Partner in Your Corner

A seasoned restoration company does so much more than just the physical cleanup. They essentially become your claim manager, working directly with the insurance company to simplify a process that can feel incredibly complicated.

They understand all the moving parts, including the actual slab leak repair, and can coordinate with the plumbers and contractors to make sure nothing falls through the cracks. This means you’re not stuck playing telephone between three different companies.

Instead of you juggling endless calls and paperwork, your restoration pro handles the documentation and communication. This turns a frantic, stressful situation into a managed, step-by-step process, letting you focus on getting your family’s life back to normal.

When you're deciding who to call, remember the right team makes all the difference. Taking a moment to find a certified water damage restoration contractor is the best thing you can do to protect both your property and your finances.

Frequently Asked Questions About Slab Leak Coverage

When you’re staring at a puddle on your floor and suspect a slab leak, a million questions race through your mind. Here are some quick answers to the most common concerns we hear from homeowners every day.

Does Insurance Cover Mold From a Slab Leak?

This is where things get tricky. Insurance coverage for mold all comes down to the source of the water. If the mold is a direct result of a sudden and accidental pipe burst that your policy covers, then your policy will likely help with the remediation, usually up to a certain dollar limit.

But if the mold grew slowly over weeks or months from a pinhole leak that went unnoticed, the insurance company will almost certainly call it a maintenance problem. From their perspective, it wasn't sudden. This is why acting fast is so important—getting things professionally dried immediately is your best shot at preventing both mold and a denied claim.

Will My Rates Go Up if I File a Claim?

It’s a very real possibility, unfortunately. Insurance carriers see water damage claims as a strong predictor of future risk. Filing even a single claim, especially for water, can trigger a premium increase at your next renewal.

This is why you have to do some quick math. Compare the total repair cost to your policy's deductible. If the damage is minor and the cost is only slightly more than your deductible, you might save money in the long run by paying out-of-pocket. It can help you avoid a rate hike or, in some cases, even prevent your policy from being non-renewed.

The bottom line is that insurance is there for major disasters. For smaller incidents, think carefully about the long-term financial impact before picking up the phone to file a claim.

Are There Special Endorsements I Can Add?

Yes, and it’s always a good idea to ask your insurance agent about them. Standard policies have gaps, but you can often buy add-ons, or "endorsements," to get more complete protection.

- Service Line Coverage: This is a big one. It can help pay to repair the water or sewer pipes running from the public main to your house—pipes that you own but that aren't typically covered.

- Equipment Breakdown Coverage: This could come into play if the leak started because a major appliance, like your water heater, catastrophically failed.

- Water Backup and Sump Pump Overflow: This is a must-have. Standard policies exclude damage from sewer backups or a failed sump pump, and this endorsement adds that coverage back in.

Just remember that even with these add-ons, the policy might not cover the cost of repairing the old, corroded pipe itself. Always read the fine print so you know exactly what you’re paying for.

When a slab leak hits, you need a team that knows how to handle everything—from the initial water cleanup to working directly with your insurance adjuster. The experts at Restore Heroes are on call 24/7 to bring professional restoration services to homeowners all across the Phoenix area. Visit us online to get the help you need now.