When you’re standing in the aftermath of a house fire, one question cuts through all the noise: Am I covered?

Let’s get right to the good news. For the overwhelming majority of homeowners, the answer is often yes. Fire damage isn’t some obscure clause or a pricey add-on; it’s one of the fundamental risks that homeowners insurance was designed to protect against from the very beginning.

Yes, Your Homeowners Insurance Likely Covers Fire Damage

If you're asking, "Does homeowners insurance cover fire damage?", you can take a small breath of relief. A standard policy is structured to be your financial first responder after a fire. It’s not just a single check for the damage, but a multi-part safety net designed to help you piece your life back together.

This protection is broken down into a few key areas that work in tandem to cover the full scope of your loss.

A Multi-Layered Approach to Recovery

Think of your policy less as a single shield and more as a complete suit of armor. Each piece protects a different aspect of your life that a fire can disrupt. The main components are:

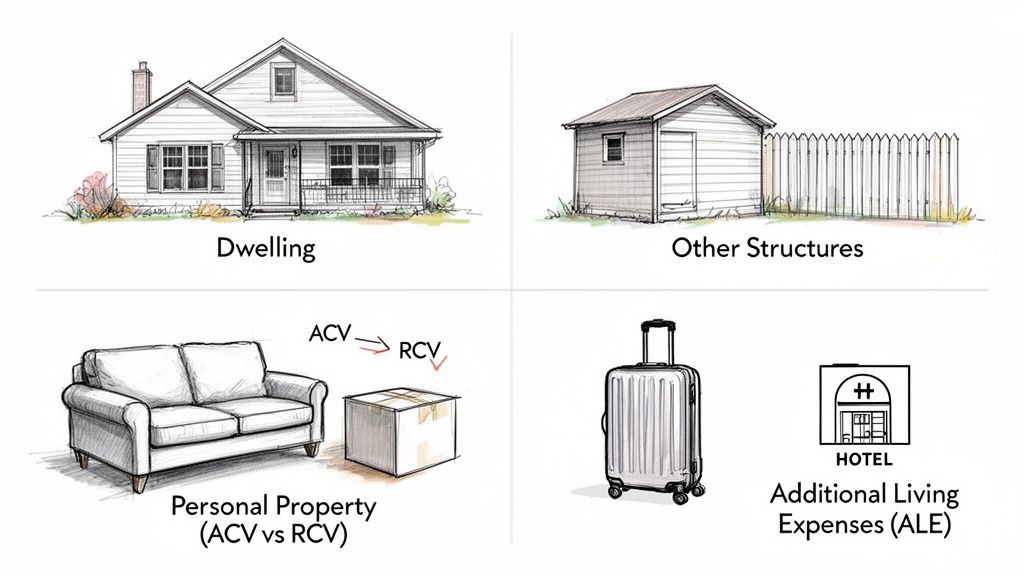

- The Structure of Your Home: This is the most obvious part. It covers the cost to repair or completely rebuild the physical house itself—from the foundation right up to the shingles on the roof.

- Your Personal Belongings: This part of your policy addresses everything inside your home. We're talking about furniture, clothing, electronics, kitchenware, and all the other possessions that make a house a home.

- Temporary Living Expenses: If the fire damage is severe enough to make your home unsafe or unlivable, this coverage kicks in. It helps pay for essential costs like a hotel stay, rent for a temporary apartment, and even the extra expense of eating out.

To give you a clearer picture, here’s a quick summary of how these standard coverages typically apply to a fire-related claim.

Standard Home Insurance Fire Coverage At a Glance

| Coverage Type | What It Typically Protects | Example Scenario |

|---|---|---|

| Dwelling Coverage | The physical structure of your house, including walls, roof, and built-in systems. | May pay to rebuild the wing of your house that was destroyed by a kitchen fire. |

| Personal Property | Your belongings, such as furniture, electronics, clothing, and other contents. | May reimburse you for the value of your smoke-damaged sofa and charred electronics. |

| Additional Living Expenses (ALE) | The cost of living elsewhere while your home is being repaired or rebuilt. | May cover your family's hotel bill and meal expenses for the months it takes to restore your home. |

| Other Structures | Separate structures on your property, like a detached garage, shed, or fence. | May pay to repair or replace a detached garage that was also damaged in the fire. |

These four pillars form the foundation of your recovery, providing resources to not only rebuild your house but also to maintain a sense of normalcy while that process unfolds.

Fire has always been one of the most significant and universal risks to a home. That's why it remains a core, foundational element of virtually every standard homeowners policy.

Historically, fire and lightning damage consistently rank among the most common and costly homeowners insurance claims filed across the country. Even as insurers grapple with increasing weather-related events, fire remains a standard covered peril. It's important to note this is unlike flood damage, which almost always requires a separate, dedicated policy. As you can learn from climate and insurance trends on APM Research Lab, the need for solid fire coverage is as critical as ever.

Now that you have the big picture, we'll dive into the specific details, including common limits, exclusions, and other policy nuances that you need to understand.

What Does Fire Insurance Actually Cover? A Closer Look

When you see "fire damage" listed on your homeowners policy, it's easy to feel a sense of relief. But in the aftermath of a real fire, what does that coverage actually translate to? It’s not just one big payout; it’s a package of different coverages, each designed to handle a specific part of the recovery process.

Think of your policy as a toolkit with four essential tools. Knowing what each one does is the key to understanding how your insurance may help you rebuild your life.

Dwelling Coverage

This is the big one. Dwelling coverage is what protects the physical structure of your house. We're talking about the cost to repair or completely rebuild everything from the foundation and walls to your roof and built-in systems like the furnace or central air.

So, if a kitchen fire scorches your walls, melts your countertops, and ruins the flooring, this is the part of your policy that may pay for those structural repairs. It’s the coverage that literally puts a roof back over your head. If you're facing this situation, you can learn more from our comprehensive article on navigating fire damage.

Other Structures Coverage

Here’s a detail many people miss: your property is more than just your house. Other Structures coverage is for buildings on your land that aren't attached to the main home.

This coverage is designed to help with damage to things like:

- Detached garages

- Storage sheds and workshops

- Fences

- Gazebos or greenhouses

If a fire starts in your home and spreads to your separate workshop, this coverage may kick in to handle those repairs. It’s typically set as a percentage of your dwelling coverage, often around 10%, but check your specific policy.

Personal Property Coverage

While dwelling coverage rebuilds the house, Personal Property coverage helps you replace your stuff—all the belongings that make a house a home. This includes everything from your sofa and television to your clothes, dishes, and kids' toys.

This is where a crucial policy detail makes a huge difference:

- Actual Cash Value (ACV): This pays you what your item was worth the moment before the fire, which includes depreciation. That five-year-old TV isn't worth what you originally paid for it, and ACV reflects that.

- Replacement Cost Value (RCV): This is often a preferred option. RCV pays the cost to buy a new, similar item at today's prices, without any deduction for age or wear and tear.

Most standard policies start with ACV. You can usually upgrade to RCV for a slightly higher premium, and in our experience, it's almost always worth it.

Additional Living Expenses (ALE)

After a serious fire, your home will likely be unlivable during repairs. This is where Additional Living Expenses (ALE), sometimes called "Loss of Use," can become a lifesaver.

ALE covers the increase in your normal living costs while you're displaced. It’s not a blank check, but it helps with expenses like:

- Hotel bills or a short-term apartment rental

- Restaurant meals if you can't cook

- Laundry services if you don't have a washer and dryer

- Pet boarding fees

This is the coverage that provides stability for your family, allowing you to maintain a sense of normalcy while we work to restore your home.

Coverage for Smoke and Water Damage After a Fire

Once the fire trucks pull away, you might breathe a sigh of relief, thinking the worst is over. But often, the flames are just the beginning. The aftermath of a fire almost always involves two other destructive forces: invasive smoke and the massive amounts of water used to put the fire out.

Many homeowners worry that their insurance only covers what actually burned. Thankfully, that’s not typically how it works. Think of it this way: the damage from smoke and firefighting efforts is considered a direct result of the fire itself. It’s all part of the same event, and your policy may see it that way, too.

The Hidden Damage from Smoke and Soot

Smoke isn't just a bad smell you have to air out. It's a physical substance made of tiny, acidic soot particles that can travel through your entire home, settling on everything you own. These particles can seep into drywall, get pulled into your HVAC system, and coat furniture in rooms the fire never even touched.

Because this damage is a direct consequence of the fire, your homeowners policy is designed to cover the cleanup and restoration. This typically includes:

- Structural Elements: Cleaning and repairing stained walls, ceilings, and contaminated flooring.

- Personal Belongings: Professionally cleaning or replacing furniture, drapes, and clothing that have absorbed soot and smoke odors.

- Air Systems: A deep cleaning of your HVAC system to get rid of trapped soot and prevent it from circulating through your home again.

A common myth is that if an item wasn't touched by flames, it's not covered. The reality is that smoke can cause just as much—if not more—widespread financial loss than the fire itself, and this is a standard part of a fire damage claim.

Water Damage from Firefighting Efforts

The sheer volume of water from fire hoses is what saves your home from being completely destroyed. But that same life-saving water introduces a brand-new problem: significant water damage. It’s important to know this is completely different from a storm-related flood, which requires a separate flood insurance policy.

Since the water was used to fight a covered peril (the fire), any damage it causes is almost always included in your fire claim. Your policy may help cover the costs for extracting the water, completely drying out the structure, and repairing anything the water ruined. Getting rid of stubborn odors is another critical step, and you can learn more about how to remove the smoke smell from your house in our detailed guide.

Important Policy Exclusions and Limits to Understand

So, while your standard homeowners policy often covers fire damage, it's not a blank check. Think of it this way: your policy is there to protect you from sudden, accidental disasters, but it has some common-sense rules and boundaries. Knowing exactly what those are before you need to file a claim can save you a world of headaches.

Most insurance is designed to cover fires that happen unexpectedly. However, there are a few key situations where your claim could be denied.

Common Fire Damage Exclusions

An insurer will likely turn down a claim if the fire wasn't truly an accident. Here are the most common reasons you might not be covered:

- Arson or Intentional Acts: This one’s straightforward. If you or someone in your household intentionally sets a fire, it’s a crime—not an insurable event.

- Vacant Homes: Insurance policies have what's called a "vacancy clause." If your home sits empty for too long, often more than 60 days, coverage might be voided. Insurers see vacant properties as higher risk, so you’d need a special type of policy to stay protected.

- Specific Named Exclusions: These are rare, but your policy will likely list certain catastrophic events that aren't covered, like fires resulting from an act of war or a nuclear hazard.

It’s also good to remember that a fire can lead to other problems. For example, all the water used to extinguish the flames can create the perfect environment for mold growth, which has its own set of coverage rules. We explain this in more detail in our guide on whether homeowners insurance covers mold.

The Growing Challenge of Wildfires

For anyone living in high-risk areas like Arizona, wildfires are an increasingly serious concern. A standard policy technically covers fire, but the massive risk from widespread wildfires has forced insurance companies to change their approach.

Wildfires pose a growing challenge to homeowners insurance coverage for fire damage, particularly in fire-prone regions. Early 2025 data from Los Angeles-area wildfires showed insurers paying over $4 billion in losses, and as a result, U.S. homeowners' premiums rose over 30% from 2020-2023. You can explore more about how climate disasters impact property insurance in this insightful government blog post.

Because of this, you might find that insurers in fire-prone states are starting to:

- Add specific wildfire exclusions to their standard policies.

- Require homeowners to buy a separate, specialized wildfire policy.

- Stop renewing policies altogether for homes located in the highest-risk zones.

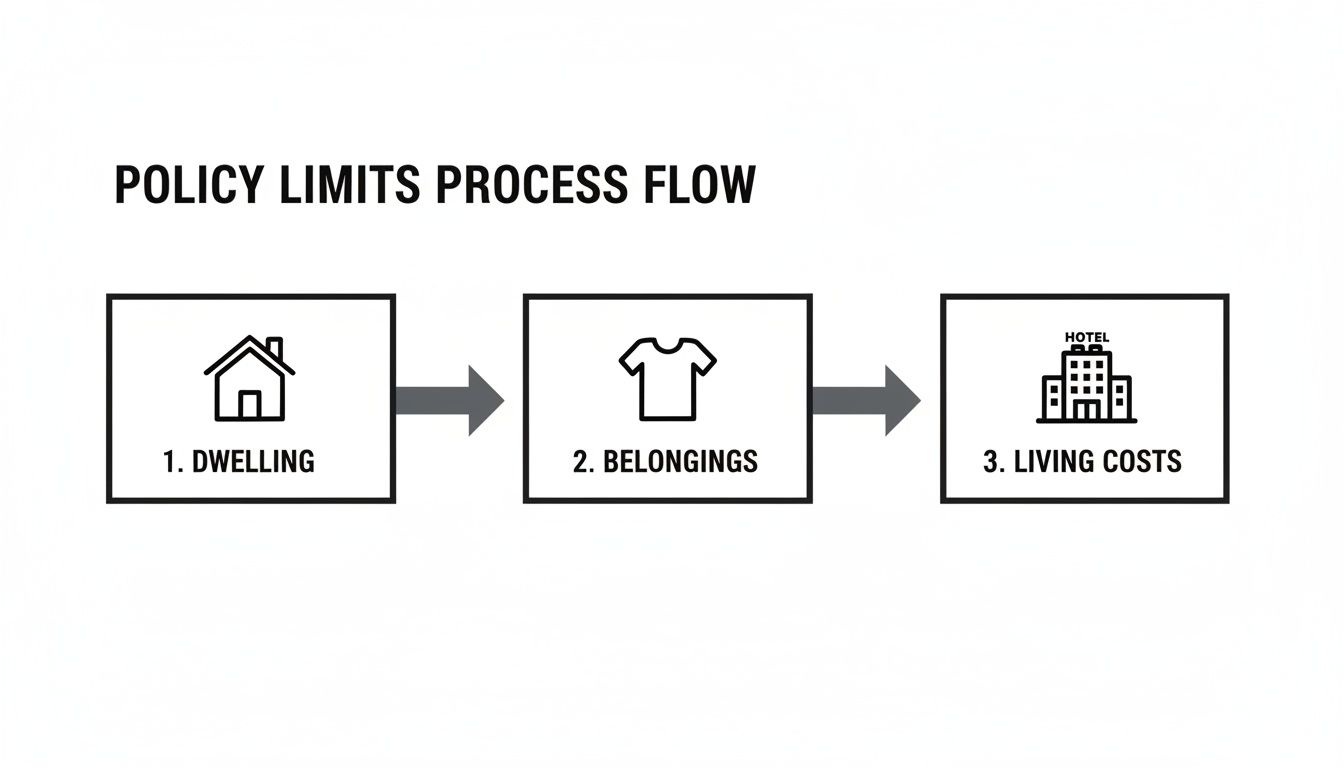

Understanding Your Policy Limits

Beyond what’s excluded, every part of your coverage has a policy limit. This is the maximum dollar amount your insurer will pay for a specific type of loss. These numbers are arguably the most important part of your entire policy, as they dictate how much financial help you’ll actually receive.

- Dwelling Limit: The total amount available to rebuild the physical structure of your house.

- Personal Property Limit: Usually set as a percentage of your dwelling limit (like 50-70%), this is the maximum you can claim for all your lost belongings.

- Additional Living Expenses (ALE) Limit: Your coverage for temporary housing and living costs might be a set dollar amount or be capped at a certain time period (like 24 months).

Make it a habit to review these limits with your agent every year. Construction costs and the value of your belongings go up, and you need to make sure your coverage is keeping pace. Being underinsured is one of the biggest roadblocks to a full recovery.

Your First Steps After A House Fire

The moments after a fire are a blur of chaos and emotion. It's completely normal to feel overwhelmed, but what you do next can make a huge difference for your family's safety and your financial recovery. Before anything else, your absolute first priority is to make sure everyone is safely out of the house.

Once the fire department has given the all-clear and the immediate danger is over, it’s time to pivot toward recovery. This process starts with a few critical first steps.

What To Do Immediately After The Fire

The actions you take in the first 24 hours set the stage for your entire insurance claim. Moving quickly and deliberately helps secure your property and protect your claim from potential pitfalls.

To help you stay on track during this stressful time, here is a simple checklist of what to prioritize.

Post-Fire Action Checklist

| Priority | Action Item | Reason |

|---|---|---|

| 1. Safety First | Confirm everyone is accounted for and safe. Get the all-clear from the fire department before even considering re-entry. | Your family's well-being is the only thing that matters. Damaged structures can be unstable and dangerous. |

| 2. Notify Insurer | Call the 24/7 claims number for your insurance company. This is the official starting pistol for your claim. | This gets an adjuster assigned to your case immediately and they will provide crucial guidance on your policy's specific rules. |

| 3. Secure Property | Contact a professional restoration company (like Restore Heroes). | They can board up windows, tarp the roof, and help prevent further damage from weather or intruders, which is often a policy requirement. |

| 4. Document It All | Take photos and videos of everything before it’s touched. Get wide shots and close-ups of all affected areas. | This visual proof is your most powerful tool. It creates an indisputable record of the damage for your claim. |

Following these steps in order will help you navigate the initial shock and start the recovery process on the right foot.

It's natural to want to dive in and start cleaning, but please, wait for approval from your insurance adjuster before you throw anything away or begin any permanent repairs.

Your homeowners policy is designed to put you back in the position you were in before the loss. Following the proper procedures is a good way to get the full benefits you're entitled to without accidentally compromising your claim.

This diagram helps visualize how your policy’s different coverage types work together to cover the structure, your possessions, and temporary living expenses.

Getting a handle on these separate "buckets" of coverage is essential for tracking your claim and making sure all your expenses are accounted for.

Preparing For Repairs And Rebuilding

As you start looking toward the future, you’ll need trusted professionals on your side. For homeowners in the Phoenix area, our team at Restore Heroes is on call 24/7 to manage the entire restoration. We handle everything from the initial damage assessment and soot removal to coordinating directly with your insurance company.

When it's time to hire a builder for major repairs, you’ll want to be prepared. Knowing the critical questions to ask a general contractor helps ensure you're partnering with someone reputable who you can trust to rebuild your home.

For a more detailed guide on navigating the entire post-fire journey, be sure to check out our complete what to do after a house fire checklist.

How a Restoration Company Works with Your Insurer

After a house fire, you're suddenly juggling two huge, stressful jobs: dealing with your insurance claim and figuring out how to manage the actual repairs. It’s a tough spot to be in, and that’s exactly where a professional restoration company comes in. We can act as the hands-on team that connects the paperwork of your policy to the real-world work of putting your home back together.

Think of us as the project managers for your recovery. While your insurance adjuster is focused on the financial side of things, we’re on the ground handling the practical side. We don't just show up with cleaning supplies; we build a detailed, evidence-based plan that gives your insurer exactly what they need to process your claim without delays. You can get a closer look at the specifics in our guide on what a restoration company does.

From Initial Inspection to Final Handover

The whole process kicks off the moment our team arrives. Our first priority is a thorough inspection to document the full scope of the fire, smoke, and water damage. This isn't just a quick walkthrough. We meticulously create a detailed scope of work using industry-standard software and techniques.

This documentation is what we use to speak the same language as your insurance adjuster. It includes:

- Detailed estimates for every single repair and cleaning task needed.

- Photos and videos that provide clear evidence of the damage.

- Moisture readings and atmospheric data to show why certain drying equipment is necessary.

By giving your insurer a professional and comprehensive damage assessment right from the start, we help cut down on the frustrating back-and-forth that can stall your claim. It helps ensure all the work needed to restore your home is accurately accounted for under your policy.

Once your adjuster approves the scope of work, we manage the entire restoration from start to finish. This covers everything from soot and odor removal to structural drying and final sanitization. We communicate directly with your insurance provider throughout, giving them progress updates and transparent invoices. Our job is to handle all that complex coordination for you, making the path from disaster back to a safe, clean home as smooth and stress-free as possible.

Common Questions About Fire Damage Insurance Claims

Even when you have a decent grasp of your insurance policy, the reality of a fire brings a flood of specific, urgent questions. After a disaster, you're not thinking in hypotheticals—you need practical answers. Let's walk through some of the most common questions we hear from homeowners in your situation.

How Does My Deductible Work?

Think of your deductible as your share of the repair cost. It's the amount you have to pay before your insurance company starts paying.

For example, if your deductible is $1,000 and the total fire damage repair bill comes to $50,000, your insurer would pay $49,000 after you've paid your deductible. The insurance company simply subtracts your deductible amount from the final settlement check they send you.

Will My Premium Go Up After a Fire Claim?

This is a common worry, and the honest answer is: it might. After you file a major claim for something like a fire, your insurance provider will re-evaluate the risk of insuring your home.

This doesn't mean an increase is guaranteed, but it is a possibility when your policy comes up for renewal.

Is a Small Kitchen Grease Fire Covered?

Yes, this is a situation homeowners insurance is often designed for. Even a small, accidental grease fire that you put out quickly can leave behind stubborn smoke and soot damage.

What might look like a simple cleanup job often requires professional remediation to fully remove odors and hidden residue, and that's something your policy is there to cover.

Of course, the best-case scenario is avoiding a fire in the first place. Taking a few minutes to learn about the common causes of house fires can give you the knowledge you need to protect your home.

A critical piece of advice: If your insurance company’s first offer seems too low, don't feel pressured to accept it. You have every right to get a second opinion and present your own detailed estimates from a restoration contractor you trust. This is a normal part of negotiating a fair settlement.

When fire, smoke, or water damage strikes your home in the Phoenix metro area, a fast response is everything. Restore Heroes is on call 24/7 to secure your property, begin mitigation, and manage the entire restoration process, working directly with your insurance provider on your behalf. For a free onsite inspection and immediate help, visit us at https://www.restoreheroesaz.com.