Water is on the tile. The baseboards are dark. Your garage smells like wet drywall, and your phone is full of missed calls from family asking what happened. In Phoenix, that moment might come from a failed water heater, an overworked AC line, a roof leak after a monsoon cell, or smoke pushing through the house after a kitchen fire.

When that happens, your homeowners policy stops being paperwork and becomes your recovery roadmap. It tells you what property is insured, how much the carrier may pay, what deductible applies, what exclusions could cause problems, and what you must do right now to protect the claim.

Most homeowners don't read the whole policy until something goes wrong. That's normal. The good news is that you don't need to become an insurance lawyer to understand how to read a homeowners insurance policy well enough to make smart decisions under pressure. You need to know where to look first, what language matters, and which mistakes tend to slow, reduce, or derail a claim.

Your Policy Is Your Recovery Roadmap

A disaster claim usually starts with confusion, not clarity. You see damaged flooring, swollen cabinets, blistered paint, or smoke residue on ceilings. You want someone to tell you two things right away. Is this covered, and what do I do next?

Your policy is where those answers begin. It's a contract, but in practical terms it's a map. It identifies the house, the people insured, the type of loss the carrier agrees to cover, the money limits attached to each category, and the conditions you have to follow after a loss.

What the policy means in real life

If a monsoon tears shingles off a roof and rain enters the attic, the policy helps answer whether the roof damage and interior water damage fall within the insuring agreement, what deductible applies, and whether temporary housing may be available if the home can't be occupied.

If a supply line bursts behind a wall, the policy often becomes the difference between an organized claim and a stressful one. The wording around sudden water damage, exclusions, mitigation duties, and mold limitations can shape every decision you make in the first day.

A useful starting point is understanding how personal lines home insurance is structured at a basic level. That context helps when you're looking at your own declarations page and trying to separate core coverage from optional endorsements.

Your policy isn't just for the insurance company. It's the operating manual for the next few weeks of your life.

Why this matters right away

When homeowners ask what a restoration company does during a claim, the answer is tied closely to policy obligations. If you want a practical breakdown, this guide on what a restoration company does helps connect emergency response, drying, cleaning, and documentation to the insurance process.

The fastest way to calm the situation is to stop thinking of the policy as one giant booklet. Read it in layers. Start with the summary page. Then review the property coverages. Then look for exclusions, endorsements, and duties after loss.

That sequence works because it matches the way claims unfold in the field. First, identify the claim. Second, check the limits. Third, make sure the loss isn't being pushed outside coverage by an exclusion or a missed condition.

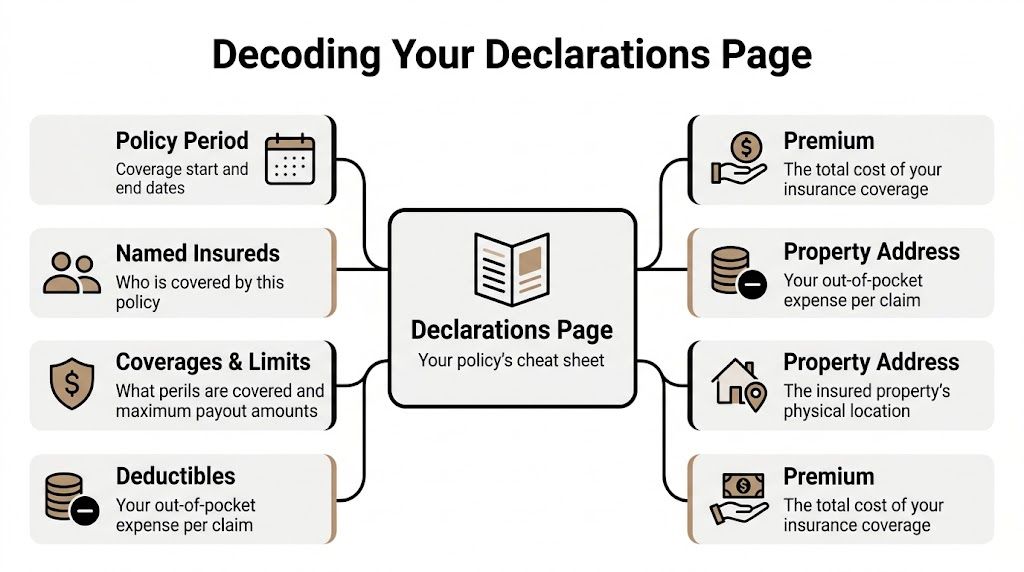

Find and Decode Your Declarations Page

After a pipe burst, a kitchen fire, or a monsoon roof leak, the declarations page is the fastest way to get your bearings. It tells you whose name is on the policy, which property is insured, what coverages were purchased, and how much of the loss you may be carrying before the carrier pays.

That page is usually short. The decisions tied to it are not.

Practical rule: Read the declarations page before you give opinions about coverage. If the names, address, limits, or deductible are wrong, the claim can stall before the adjuster even gets to the damage.

Confirm the policy is tied to the right house and the right people

Start with the identity details. This sounds basic, but I have seen claims slow down over simple errors that should have been caught in two minutes.

Check these first:

- Policy number. Keep it in front of you for every call and email.

- Policy period. The date of loss has to fall within the active term.

- Named insureds. Make sure the homeowner names are complete and correct.

- Property address. Confirm the insured location matches the damaged home.

In Phoenix, this matters more than people expect. Vacation properties, rental conversions, and recent moves can create confusion fast. If the carrier sees a mismatch between the loss address and the insured address, that can trigger extra review right when you need drying, board-up, or cleanup approved.

Read the coverage table for today's decisions

The coverage table is the part of the declarations page you will use during the first calls on the claim. It shows the major coverage categories and the limits attached to each one. Those numbers are caps, subject to the rest of the policy. They are not promises that every dollar of damage gets paid.

Focus on the entries that affect emergency response and housing:

- Dwelling coverage

- Other structures

- Personal property

- Loss of use

- Liability and medical payments

Read carefully for separate deductibles. Many Phoenix homeowners assume every loss hits the same deductible, then get surprised when wind or hail is handled differently from a plumbing leak. That changes whether it makes sense to file, how you budget for mitigation, and how hard you push for scope accuracy early.

Endorsements matter here too. If the declarations page lists added forms or special limits, flag them. Those short codes can change how water damage, ordinance and law, sewer backup, or roof settlement is handled.

Moisture claims are a common trouble spot in the Valley because heat accelerates deterioration and delays can turn a clean water loss into a mold dispute. Before you talk through that issue with the adjuster, review this breakdown of whether homeowners insurance covers mold.

A short visual review can help if you're looking at the page for the first time:

Mark these items before you call the carrier

Do not read the declarations page passively after a loss. Mark it up.

Circle or highlight these items:

- The deductible amount. This tells you your likely out-of-pocket share before insurance starts paying.

- Every listed endorsement. Added forms often change the standard policy language.

- The dwelling limit and loss-of-use limit. Large fire and water losses can put pressure on both.

- The policy form name. That helps explain whether your contract is broader or narrower than you expected.

- Any special percentage deductibles or peril-specific deductibles. These can change the math quickly on storm-related claims.

The declarations page will not explain exclusions, valuation rules, or all of your post-loss duties. It does tell you what policy is in force and where the main financial boundaries start. In a real emergency, that is enough to keep you from making blind decisions in the first 24 hours.

Breaking Down Your Property Coverages

Most of the repair work after a disaster falls under Section I, the property portion of the policy. In this section, the policy separates the house itself from detached structures, contents, and temporary living costs. If you understand these four buckets clearly, conversations with the adjuster get much easier.

For Phoenix homeowners, the biggest mistake isn't always lack of coverage. It's misunderstanding which bucket a loss belongs in.

The four coverages that drive most residential claims

| Coverage | What It Protects | Common Phoenix Example |

|---|---|---|

| Coverage A | The dwelling itself | Drywall, flooring, cabinets, and framing damaged after a burst pipe inside the home |

| Coverage B | Other structures on the property | A detached workshop or block wall damaged in a monsoon event |

| Coverage C | Personal property | Smoke-damaged electronics, furniture, clothing, and household items |

| Coverage D | Loss of use or additional living expense | Hotel and related living costs while the home is being dried or rebuilt after a covered loss |

Coverage A and the actual structure

Coverage A, often called dwelling coverage, is the core of the policy for structural losses. It applies to the house itself and attached structures. In real terms, this usually means the roof system, interior walls, flooring, built-in cabinetry, insulation, and attached garage areas.

In Phoenix, this coverage gets tested by sudden water losses, kitchen fires, and storm-related roof entry. If an upstairs supply line fails and water runs through drywall into the first floor ceiling, Coverage A is where the structural side of that claim usually starts.

According to The Zebra's homeowners policy guide, a useful benchmark for dwelling coverage in Phoenix is $300-500 per square foot. The same source notes that underinsurance hits 60% of claims, which is why an old coverage limit can become a serious problem after a major rebuild.

Coverage B and detached structures

Coverage B protects structures that aren't attached to the home. In Phoenix, that might mean a detached garage, shed, fence line, or workshop.

This coverage often gets overlooked until a storm takes down part of a detached structure or fire spreads beyond the main residence. Homeowners remember the roof and drywall inside the house. They forget the detached casita wall, the exterior gate system, or the separate storage building until estimate time.

That oversight matters because detached structures don't automatically draw from the same bucket as the dwelling.

Coverage C and everything you own inside

Coverage C, or personal property, is where contents claims live. This includes clothing, furniture, electronics, kitchenware, linens, and many other belongings damaged by a covered event.

Smoke claims often expose how hard this category is to manage. Homeowners can see blackening around vents and soot film on surfaces, but they may miss how far odor and residue traveled into drawers, closets, and soft goods. Water losses create the same problem with cabinets, stored items, rugs, and electronics.

If you're dealing with a plumbing failure, this guide on whether homeowners insurance covers busted pipes is a helpful companion because it separates the pipe event from the damage caused by that event. Those are not always treated the same way.

Contents claims are won or lost on detail. The carrier doesn't know what was in the closet, the garage cabinet, or the media room unless you document it.

Coverage D and living somewhere else for a while

Coverage D, often called loss of use or ALE, helps when a covered loss makes the home unlivable. In practice, this may include temporary housing and related necessary expenses while repairs are underway.

The Zebra notes that standard policies often provide 20-30% of dwelling coverage for ALE, and daily limits of $200-500 can be restrictive during a 30-90 day restoration in a serious claim. The same source says that proper declarations page review can boost full payout rates by 75%, largely because homeowners catch these caps before they commit to expenses that may not fit the policy.

This matters in Phoenix because a home can become unlivable quickly in summer. A loss that affects water service, HVAC performance, or large areas of flooring and drywall isn't just inconvenient. In high heat, it can make occupancy unrealistic.

Replacement cost versus actual cash value

A policy doesn't just say what is covered. It also says how losses are valued. That is where homeowners often discover the difference between replacement cost value (RCV) and actual cash value (ACV).

RCV aims to pay the cost to replace with like kind and quality, subject to the policy terms. ACV factors in depreciation. If the damaged flooring, cabinets, or contents are older, ACV can leave a bigger gap between what the carrier pays and what the replacement costs.

In plain language, RCV is usually the stronger position after a serious loss because it tracks more closely to what restoration and rebuilding cost today. ACV can feel manageable on paper until you price out materials, contents replacement, and labor in practice.

What works and what doesn't

What works:

- Reading each property category separately so you don't assume one limit covers everything.

- Matching damaged items to the right bucket before you submit inventories or estimates.

- Checking valuation language early so you know whether depreciation will affect your recovery.

- Reviewing ALE rules before booking temporary housing.

What doesn't:

- Lumping structure and contents together in one undocumented total.

- Assuming every water loss is treated the same way.

- Ignoring detached structures until late in the estimate process.

- Treating coverage limits as guaranteed claim checks.

The practical goal is simple. Tie each damaged thing to the policy category that governs it. That's how you turn a stressful loss into a claim file the carrier can process.

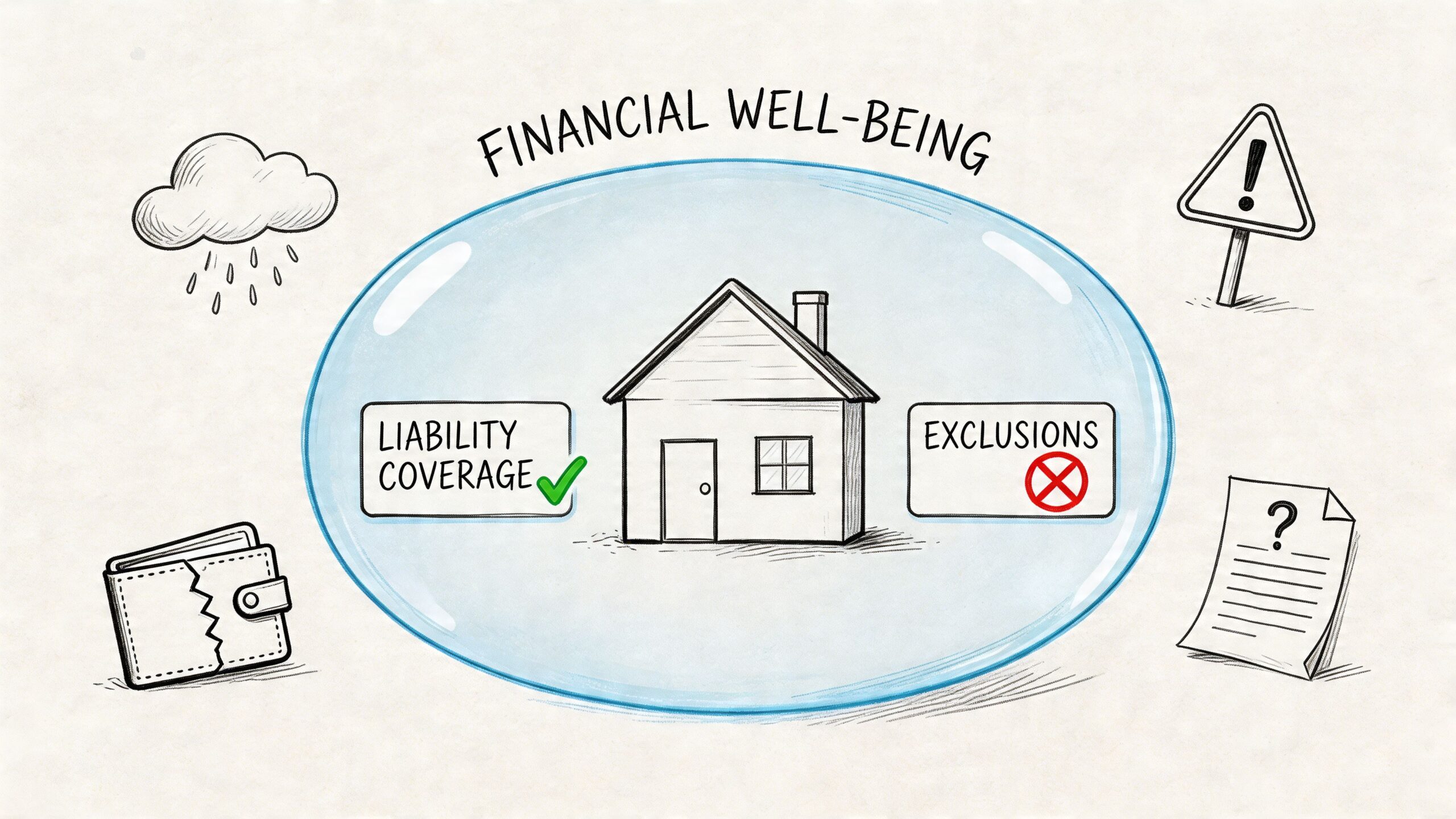

Understanding Liability Endorsements and Exclusions

Property coverage gets most of the attention after a disaster, but Section II matters too. It deals with liability, which can become important if another person is hurt in connection with the loss.

A common example is a guest slipping on a wet floor after a leak or being injured by debris during an emergency. In that situation, the issue isn't rebuilding drywall. It's whether the policy's liability coverage responds to allegations that the homeowner is legally responsible.

Exclusions decide more than most homeowners expect

If the declarations page is the summary, the exclusions section is the reality check. In this section, the policy states what it does not cover, limits sharply, or covers only under narrow conditions.

The most important distinction for Phoenix homeowners is the difference between flood and water damage inside the home from a sudden event. A standard homeowners policy commonly treats those very differently. Water entering from a burst pipe, failed appliance line, or other sudden internal event may fit one path. Widespread rising water from outside typically fits another.

That distinction matters in the desert more than people expect. Phoenix homeowners sometimes assume flood risk belongs only to other regions. Then a strong monsoon cell pushes water where it has no business going, and the policy language suddenly matters a lot.

Endorsements change the standard policy

An endorsement changes the base policy. It can add coverage, narrow coverage, or modify the way a particular claim is handled. You can't safely read the policy without checking which endorsements are attached.

According to Property Insurance Coverage Law's guide to reading a policy, 30% of water claims are denied for "continuous seepage" being misread as a covered sudden event. The same source says failure to comply with the duty to mitigate can void 25% of claims, and notes that ordinance or law coverage is a common rider that can address 10-25% of rebuild cost for code upgrades after a fire.

A strong claim can still run into trouble if the loss is excluded, the damage developed too gradually, or the homeowner didn't act fast enough to prevent further damage.

Three problem areas to review carefully

Continuous seepage versus sudden discharge

This is one of the biggest claim disputes after water damage. If the carrier sees long-term leakage, staining, rot, or conditions that suggest the problem wasn't sudden, coverage can tighten quickly.Mold and related contamination limits

Mold may be covered only in limited circumstances, and often only when it follows a covered event and is handled promptly. Even then, sublimits and endorsements can control how far the policy goes.Ordinance or law coverage

Older Phoenix homes can run into current code requirements during rebuilding. If parts of the home must be brought up to code after a covered loss, this endorsement can become very important.

Conditions are not fine-print trivia

The policy also imposes duties on the homeowner. These can include giving prompt notice, protecting the property from further damage, keeping records, cooperating with the investigation, and showing damaged property when requested.

That duty to mitigate is a live issue on almost every restoration claim. If a pipe burst saturates drywall and padding, waiting too long to extract water, remove wet materials, or begin drying can make the damage worse. Carriers often look closely at that timeline.

What works is straightforward. Stop further damage, document the scene, preserve damaged items when appropriate, and keep communication organized. What doesn't work is assuming the insurer will sort everything out later while the property sits wet, smoky, or unsecured.

Navigating the Claims Process After a Disaster

At 2 a.m. during a Phoenix monsoon, water starts pushing in around a window, the ceiling stains spread, and the panic sets in fast. By sunrise, the claim is already being shaped by what you did in those first few hours.

Your policy tells you what may be covered. Your actions help prove the loss, show that you protected the property, and keep a bad situation from turning into a claim dispute.

The first 24 hours matter most

Start with safety. If you have exposed wiring, active leaking near electrical fixtures, structural movement, sewage, or heavy smoke, get out and wait for the right help.

Once the property is safe to enter, focus on stabilization. In Phoenix, heat accelerates damage. Wet drywall, insulation, and cabinets do not sit still in a 110-degree environment. Smoke odors also sink deeper when the house stays closed up and hot.

Handle the first day in this order:

Stop the source if you can do it safely

Shut off the water to a failed supply line or appliance. If a storm opened the roof, use emergency tarping or board-up if conditions allow.Report the loss to the carrier

Get the claim number, the adjuster contact if available, and clear instructions on any immediate documentation they want.Document the scene before cleanup changes it

Take wide shots first, then close-ups. Photograph the source area, affected rooms, flooring transitions, ceiling stains, damaged contents, and any visible point of entry.Start a written timeline

Note when the loss happened or when you discovered it, who you spoke with, what emergency work was done, and when.Save receipts and work authorizations

Keep every invoice for tarping, extraction, board-up, temporary repairs, lodging, and supplies tied to the loss.

Good documentation is plain and repetitive. That is exactly why it works.

Build a claim file the adjuster can follow

A clean claim file reduces confusion and cuts down on back-and-forth. The adjuster was not there when the loss happened. Your file needs to show the condition of the property, the timeline, and the steps taken to prevent further damage.

Keep these items together in one digital folder if possible:

- Photos and video of all affected areas, not just the worst room

- A room-by-room contents list with brand, approximate age, and condition if known

- Receipts for emergency services and temporary living costs

- A call log with dates, names, and short notes from each conversation

- Moisture and drying records if mitigation work was performed

- A copy of the relevant policy pages so you can compare what happened to what the policy says

Contents claims often stall because homeowners know what they lost but cannot show it clearly. The structure is easier to see. Personal property takes more work. If you can match damaged items to photos, old receipts, owner manuals, or even prior listing photos from a refinance or sale, that helps.

Know who does what

The adjuster determines coverage for the carrier. The restoration contractor documents conditions, stabilizes the property, and performs mitigation and repair work within the approved scope or the documented need.

Those are different jobs.

On a water loss, field records can make a real difference. Moisture readings, thermal imaging, equipment logs, and daily drying notes help show what was affected and why certain materials had to come out. On a storm loss, close-up roof photos, elevation notes, and interior leak mapping matter for the same reason. If you are dealing with roof damage, this guide to winning a hail damage roof insurance claim gives a useful view of how that documentation is built.

Speak clearly and avoid avoidable claim problems

Keep your description factual. State what you know, when you found it, what you did right away, and what areas were affected. Do not guess about hidden damage or technical cause if no one has confirmed it yet.

For example, "We found water coming from the supply line under the sink at 6:30 p.m., shut off the house water, moved contents, photographed the kitchen and adjacent rooms, and had extraction started that night" is much stronger than a broad statement that the whole house is ruined.

For water losses, these water damage insurance claim tips for Arizona homeowners line up well with what carriers and mitigation teams usually need to see early.

What slows a Phoenix claim down

Some delays are unavoidable. Many are not.

The problems we see most often are late reporting, delayed mitigation, incomplete contents lists, missing receipts, and descriptions that overreach what the visible evidence supports. Another common issue in Phoenix is weather-related confusion. Wind-driven rain, roof damage, outside drainage, and long-term wear can look similar to a homeowner in the moment, but they do not get handled the same way under the policy.

Stay organized. Be accurate. Protect the property fast.

That approach does not guarantee payment, but it gives the carrier a documented file, a clear timeline, and fewer reasons to question what happened or why emergency work was necessary.

Phoenix Homeowner Policy FAQs

Phoenix claims often turn on a few questions that don't get answered well in short policy summaries. These are the ones homeowners usually ask when the damage is already in front of them.

Do I need separate flood insurance in Phoenix

Often, yes. A standard homeowners policy commonly does not cover flood damage from outside water entering on a broader flooding basis. That's why desert assumptions can be expensive. Phoenix may be dry most of the year, but monsoon runoff and sudden street or lot drainage problems can create a very real coverage gap.

If your property has any history of drainage trouble, low entry points, or water movement from outside toward the structure, this is worth discussing with your insurance professional before the next storm season.

What is ordinance or law coverage

This endorsement helps when rebuilding after a covered loss triggers code-related upgrades. The base policy may pay to repair direct damage, but current building requirements can add cost beyond simple replacement of what was there before.

That matters more in older homes. If electrical, structural, or other components must be updated to meet current code during rebuilding, ordinance or law coverage can become one of the most valuable parts of the policy.

What's the difference between a company adjuster, an independent adjuster, and a public adjuster

A company adjuster works for the insurance carrier. An independent adjuster is typically assigned by the carrier but isn't a direct employee. A public adjuster works for the policyholder, not the insurer.

The key point is to know who you're speaking with and who they represent. That helps set expectations about their role in the claim.

Does fire damage include smoke damage

It can, but the scope matters. Fire claims aren't only about charred framing or open flame. Smoke, soot, odor, and corrosive residue can affect cabinets, HVAC systems, electronics, textiles, and painted surfaces far from the burn area.

If you're sorting through that issue, this guide on whether homeowners insurance covers fire damage can help you frame the claim more accurately.

What's the single biggest mistake after a loss

Waiting too long to act. Not because every delay ruins a claim, but because wet materials, smoke residue, and heat-related conditions don't pause while paperwork catches up.

The better approach is simple. Read the declarations page first. Identify the coverage bucket involved. Check exclusions and endorsements. Then document everything and mitigate further damage right away.

If your Phoenix home has suffered water, fire, smoke, mold, or biohazard damage, Restore Heroes can help you stabilize the property, document conditions, and move the restoration process forward with clear communication. When you're dealing with a stressful loss, having an experienced local team involved early can make the path from damage to recovery much easier to manage.