A burst pipe hits before sunrise. By mid-morning, your office carpet is soaked, drywall is swelling, and the smell has already changed. Or maybe it's a kitchen fire in Scottsdale that leaves smoke residue in the vents and shuts down dinner service for days. The visible damage gets your attention first. Then the harder truth sets in. Your income has stopped, but your obligations haven't.

Rent is still due. Payroll questions start immediately. Vendors want updates. Customers need answers. If you run a retail store, restaurant, clinic, warehouse, or service business in the Phoenix area, a property loss can turn into a cash-flow crisis fast.

That's where business interruption coverage matters. It isn't about fixing drywall, replacing flooring, or cleaning soot. Property coverage usually addresses the physical repairs. Business interruption coverage is built for the money side of the loss, the gap between the day your doors close and the day normal operations can resume.

Many owners don't think about it until they need it. That delay can be costly. Studies by the Federal Emergency Management Agency indicate that 90% of businesses fail within a year if they cannot resume operations within five days after a disaster, yet only 30-40% of small business owners carry business interruption insurance according to the NAIC overview of business interruption coverage.

When Disaster Strikes Your Phoenix Business

At 6:30 a.m., a Phoenix business owner opens the door and knows within seconds the day is off track. Water has spread across the floor from a broken line in the wall. Displays are swollen. Boxes at ground level are soft. The space may be repairable, but it is not ready for customers.

A fire loss can look different and create the same business problem. A restaurant in Scottsdale might have limited burn damage in one part of the building, yet smoke residue in the dining area, bar, and HVAC system can still stop service. For a clinic, office, or retail store, the issue is often safety first, then access, then time.

That time is expensive.

A property loss usually creates two tracks of damage at once. One is the building and contents you can see. The other is the income you stop earning while fixed costs keep coming. Owners feel that pressure fast. Rent does not wait. Payroll questions start the same day. Customers want clear answers about when you will reopen.

For severe water losses, the first smart move is often immediate mitigation and documentation, not guesswork about the final repair bill. Drying equipment, moisture readings, photo records, debris removal, and salvage decisions all help shape what happens next. That is why many local businesses call for commercial water damage restoration support as soon as the property is safe to enter.

Restoration work also affects the insurance side more than many owners expect. If your policy requires you to protect the property from further damage, a qualified restoration team helps you meet that duty. Just as important, their records can help show when the damage happened, what steps were taken to reduce it, and how the closure period developed. In a real claim, that paper trail can matter almost as much as the drying or cleanup itself.

A closure often starts as a cleanup problem and becomes a cash-flow problem within days.

Business interruption coverage is built for that gap. It can help replace lost business income after a covered physical loss forces your operations to slow down or stop. This coverage is the difference between absorbing weeks of lost revenue alone and having insurance step in while repairs and restoration move forward.

If you want a plain-language overview before getting into policy details, this guide on understanding business interruption insurance is a helpful starting point.

For a Phoenix business owner, the practical question is not only, “What got damaged?” It is also, “How do I reopen as quickly as possible, document every step, and avoid mistakes that give the carrier a reason to question the loss?” That is why restoration and insurance should never be treated as separate tracks after a disaster.

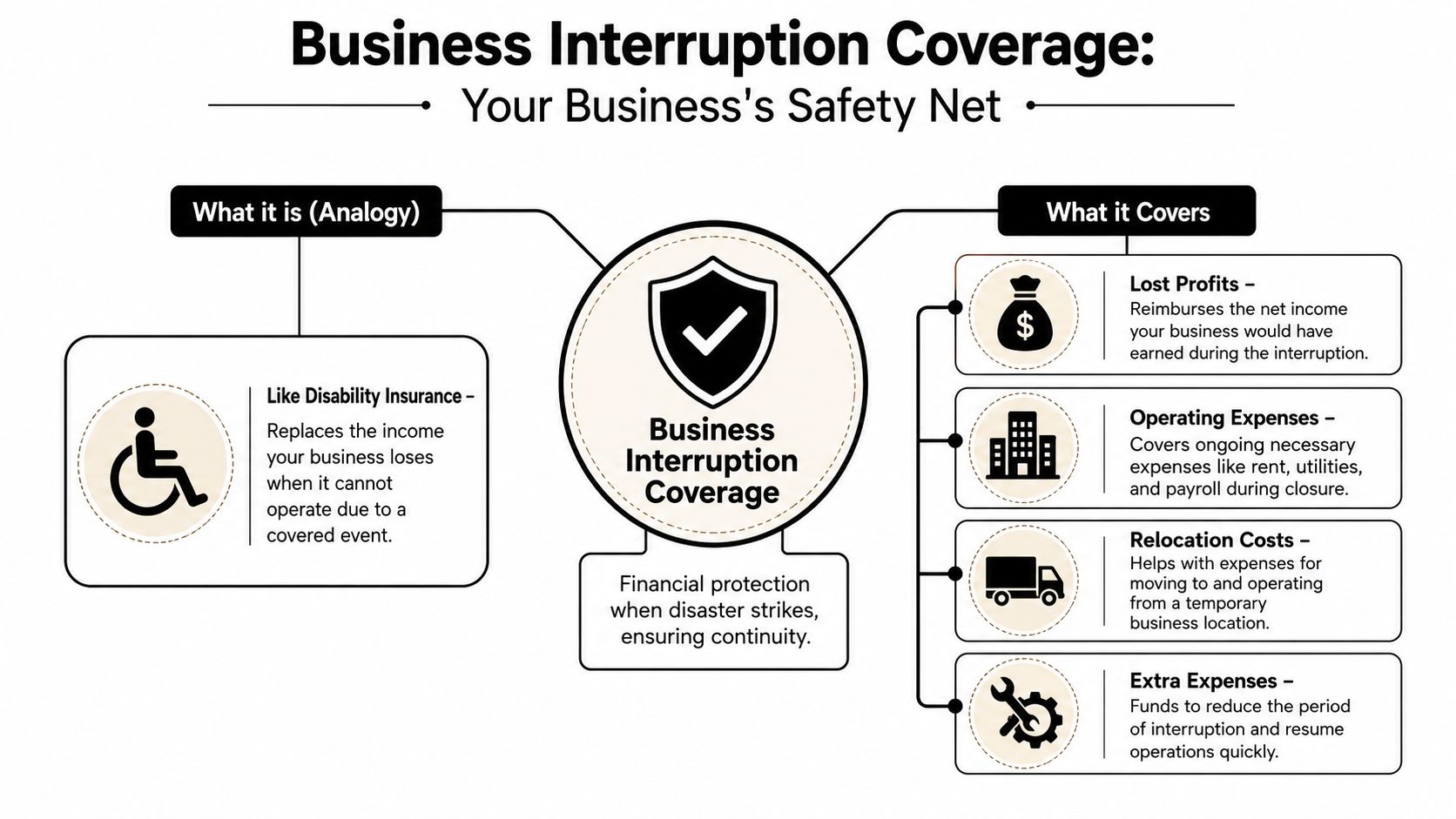

What Exactly Is Business Interruption Coverage

Think of business interruption coverage as disability insurance for your company's income. If a covered property loss leaves your business unable to operate, the policy may step in to replace part of the income stream the business would have generated during the shutdown.

That simple idea helps, but the policy only works when a specific trigger is met. Most standard policies are triggered only by “direct physical loss or damage” to insured property. They compensate for lost net income and continuing fixed expenses like rent and taxes that persist even when operations are suspended according to this guide on business interruption insurance coverage basics.

The trigger that confuses most owners

Many people often misinterpret the conditions. A slowdown in sales is not enough by itself. A hard month in business is not enough. A government restriction, supplier delay, or neighborhood issue may not be enough either unless your policy has specific language that applies.

What usually starts the analysis is tangible damage at the insured property. Fire damage, storm damage, vandalism, or water damage from a covered cause are the kinds of events owners often think about here.

Here's the practical test:

| Situation | Usually the first question |

|---|---|

| Fire in your building | Did it cause direct physical damage? |

| Pipe burst in your suite | Did the water physically damage insured property? |

| Sales dropped with no property damage | Was there any direct physical loss at all? |

| Local shutdown with no building damage | Does the policy have any special endorsement? |

Two policy terms worth knowing

Owners don't need to become adjusters, but two terms help a lot.

- Indemnity means the insurer is trying to put the business in roughly the financial position it would've been in if the covered loss hadn't happened.

- Period of restoration means the repair-and-recovery window during which the policy may respond, subject to the policy language.

If you want a second plain-English reference, PTL Insurance Associates has a useful piece on understanding business interruption insurance that helps frame the coverage in business-owner terms.

Why documentation starts on day one

Once the trigger is met, the claim becomes a documentation exercise as much as a repair issue. That's why owners often need both financial records and property-loss records moving in the same direction. Good photo logs, drying records, repair scopes, and communication history can support the claim file from the start. Many businesses also look for insurance claim assistance when the paperwork starts to pile up.

Practical rule: If there's no covered physical damage, business interruption coverage often never gets off the ground.

Key Coverages and Common Exclusions

A standard business interruption claim usually has two sides. One side is what the policy may pay. The other is what the policy won't touch unless separate coverage or endorsements apply. Owners need both sides to read the situation correctly.

What the policy may cover

The first bucket is lost net income. That's the earnings the business would likely have made if the covered property loss had not happened.

The second bucket is continuing operating expenses. Some costs don't disappear just because the doors are closed. Depending on the policy terms, these may include items such as rent, mortgage obligations, taxes, and insurance-related costs that still come due during the interruption.

A third bucket often matters in real-world recovery more than owners expect. Extra expense coverage can apply to reasonable costs spent to reduce the interruption period. That could mean setting up temporary operations, paying for expedited services, or making short-term adjustments that help the business function sooner.

The supplier and customer issue

Some owners assume their policy only matters if their own building is damaged. That's not always the whole picture.

Standard business interruption policies typically exclude losses from pandemics, floods, and earthquakes. They also do not cover income loss unless a dependent supplier or customer suffers direct physical damage, a protection known as contingent business interruption coverage, as explained in Investopedia's summary of business interruption insurance.

That contingent coverage matters if your business depends heavily on one manufacturer, one warehouse, or one major customer site. But it usually has to be specifically supported by the policy wording and documentation.

What surprises people most

Owners often expect “business loss” insurance to respond to any event that hurts revenue. That expectation causes frustration later. Common surprise areas include:

- Flood losses: Standard business interruption coverage often won't apply unless the underlying property damage itself is covered.

- Earthquake damage: Same issue. The cause of loss matters.

- Pandemic-related shutdowns: These are commonly excluded under standard forms.

- Utility or access problems: These may be limited or excluded unless the policy says otherwise.

- Undocumented income: If sales records are thin or inconsistent, proving the loss becomes much harder.

If the underlying property loss falls outside the policy, the income claim usually falls with it. Business owners dealing with water events often start by sorting out whether the water source is typically covered, and resources on whether insurance covers water damage can help frame those first questions.

Coverage is rarely decided by the size of the disruption alone. It's decided by the cause of loss, the policy wording, and the records behind the claim.

How Your Lost Income Is Calculated

Most owners hear “lost income” and assume the insurer just looks at the days the doors were closed and multiplies that by average sales. It's usually more careful than that.

The basic idea is to estimate what your business would have earned if the loss never happened, then account for the expenses that stopped during the closure. The policy is focused on net income, not gross revenue by itself.

The simple version of the math

A practical way to think about it is:

Projected revenue minus expenses that stopped because of the shutdown equals the covered net income loss

That means the claim review often looks at two sets of numbers at the same time:

- Money you likely would have brought in

- Costs you didn't have to pay because operations were reduced or paused

The records that usually matter most

Insurers often compare pre-loss performance with the interruption period. That may include:

- Profit and loss statements: These help show normal income patterns.

- Tax returns: They provide a broader financial history.

- Sales reports: Useful for seasonal businesses or companies with strong weekly patterns.

- Payroll records: These help show what labor costs continued.

- Vendor invoices and operating bills: These can show which expenses stopped and which didn't.

A business with strong bookkeeping usually has a cleaner path here. A business with scattered records often spends extra time rebuilding the story after the loss.

The trigger still matters before the math starts

No matter how good your financial records are, the coverage question still comes first. A fundamental requirement of business interruption coverage is the “physical loss” trigger. Mere access restrictions or government shutdowns without tangible property destruction are insufficient to activate compensation for lost income, as explained in FindLaw's discussion of the physical loss requirement.

That's why a realistic repair schedule matters too. The projected reopening window affects how long the interruption may be evaluated. Owners often ask early how long drying, demolition, cleaning, or rebuild work may take, and even a rough project completion timeline can help tie operations planning to the financial side of the claim.

Your Duties and the Claims Process After a Loss

The first day after a property loss is chaotic. People want answers before you have them. Staff wants direction. Customers want updates. Your insurer wants notice. Meanwhile, the building may still be getting worse if water, smoke, or contamination isn't controlled.

A claim tends to move better when the owner treats it like two parallel jobs. One job is emergency response at the property. The other is building a clean claim file.

Here's a practical sequence that keeps both moving.

The first actions that matter most

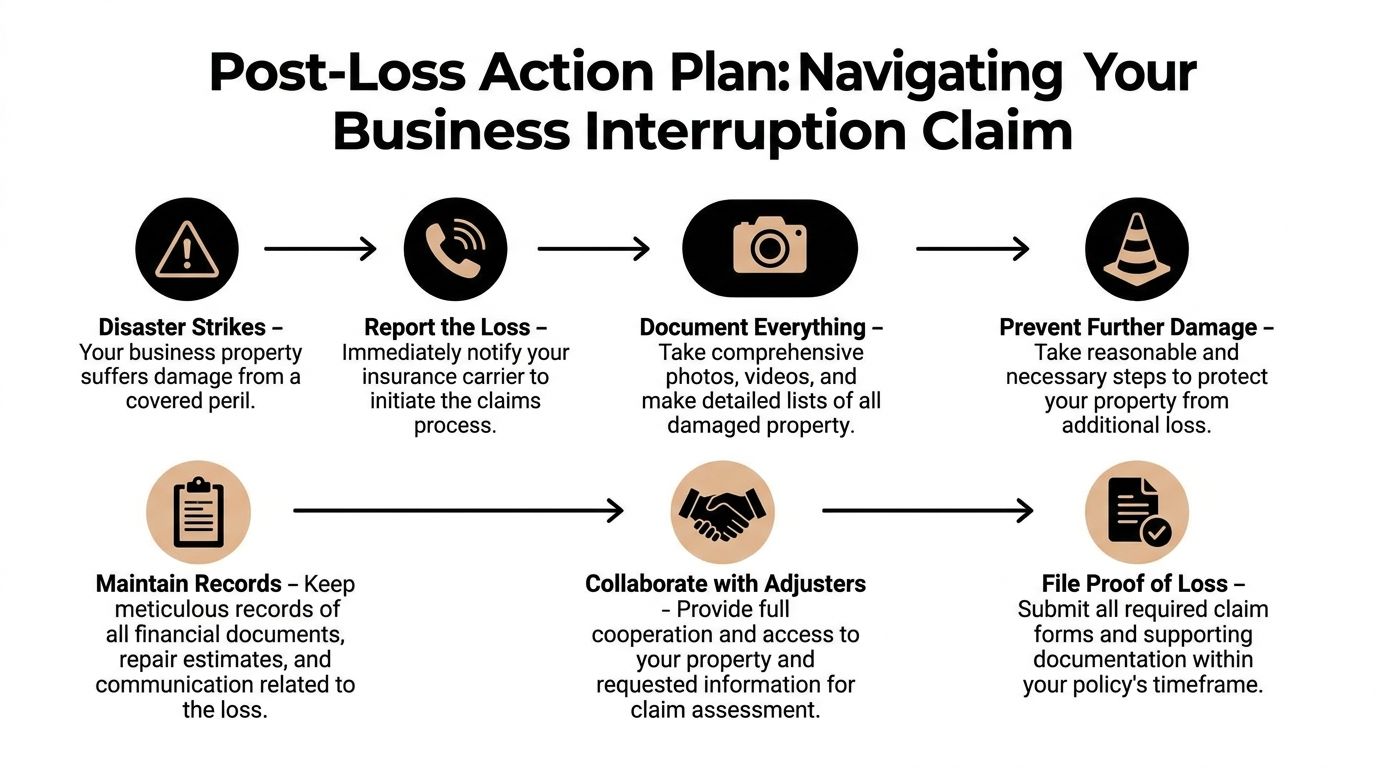

Protect the property from further damage

If water is still flowing, shut it off. If the fire department has cleared the site, secure openings and stabilize conditions where it's safe to do so. Insurers usually expect owners to take reasonable steps to prevent the loss from getting worse.Notify the insurance carrier promptly

Don't wait until every receipt and photo is organized. Start the notice process early so the claim file exists and the adjuster can begin.Document the scene before cleanup changes it

Take photos and video of affected rooms, equipment, finishes, inventory, and exterior conditions if relevant. Make notes on when the event was discovered and what immediate steps were taken.Separate property damage records from income loss records

Keep repair estimates, emergency service invoices, and moisture logs in one lane. Keep sales reports, payroll, booking cancellations, and operating costs in another.

For property owners who feel overwhelmed by insurance paperwork, even consumer-facing guides on how to file a homeowners insurance claim can still help reinforce the habit of early notice, careful records, and organized communication.

The waiting period trips people up

Business interruption coverage usually doesn't begin the minute the loss occurs. Many policies apply a waiting period that works like a time-based deductible. That means very short interruptions may not generate payable income loss even if the event itself is covered.

This catches owners off guard because the shutdown feels immediate, but the policy's income component may start later than the physical response work.

Keep a daily timeline from the first hour of loss. Write down who you called, what was damaged, what areas were unusable, and what changed each day.

Cooperation is part of the job

The adjuster may ask for financial statements, repair records, lease documents, tax filings, photos, and vendor information. Slow responses don't always sink a claim, but they often create avoidable delays.

Some businesses now use digital tools to sort invoices, forms, and claim records faster. If you're curious how document-heavy claim workflows are changing, this overview of how teams streamline insurance claims with AI gives useful context.

A short explainer can also help staff understand the flow before meetings with the carrier:

Common Claim Pitfalls to Avoid

Many business owners assume the hard part is proving there was damage. In practice, one of the hardest parts is proving how the policy language applies to the way the business operated during the interruption.

That's especially true when the business didn't go fully dark.

Partial shutdown can become a major dispute

A store may stay open but lose half its selling space after water damage. A restaurant may offer takeout but lose dine-in service because of smoke contamination. A medical office may still answer phones while treatment rooms remain unusable.

Owners often think, “We were clearly interrupted.” Insurers may ask a narrower question: “Were operations suspended in the way this policy requires?”

A frequent reason for claim denial, affecting up to 68% of disputed cases, is the insurer's interpretation that operations were only “partially impaired” rather than fully “suspended,” a nuance many policyholders are unaware of, according to United Policyholders' guidance on business interruption claim disputes.

Other mistakes that weaken a claim

Some problems are less dramatic but just as costly.

- Thin financial support: If your books can't show normal revenue patterns, the income claim becomes harder to prove.

- Poor scene documentation: Once demolition or cleanup starts, some evidence disappears for good.

- Mixed records: If emergency invoices, payroll questions, inventory losses, and repair notes all live in one messy email chain, important details get missed.

- Missed policy deadlines: Proof-of-loss timing and document requests matter.

- Assumptions about coverage: Owners sometimes act as if any closure automatically qualifies, then discover the policy language is narrower.

A better way to frame the claim

Don't just say the business “suffered.” Show exactly what changed.

Use operational facts:

- which rooms became unusable

- which services stopped

- which equipment was down

- which staff functions were interrupted

- which dates mark each phase of restricted operations

“Partially open” can still mean materially interrupted, but you need records that show what the business could no longer do.

That level of detail won't rewrite the policy, but it gives the claim a firmer factual foundation.

How a Phoenix Restoration Pro Can Help Your Claim

Business interruption claims live at the intersection of property damage, timing, and documentation. That's why the cleanup side and the insurance side can't really be separated after a serious loss.

A professional restoration team helps first by addressing the owner's immediate duty to reduce further damage. Fast extraction, structural drying, soot cleanup, containment, and dehumidification can protect the building from avoidable secondary damage. Just as important, those actions create a record of what conditions existed and what had to be done.

Why the paperwork matters almost as much as the cleanup

Adjusters usually need more than a verbal description. They often look for photo documentation, moisture readings, drying logs, demolition notes, equipment placement records, and repair-related observations. A restoration contractor who documents carefully gives the owner a stronger operational history of the loss.

That doesn't guarantee payment, and it doesn't replace policy review. It does make the claim easier to understand and harder to misstate.

Why local experience helps

Phoenix-area losses bring local realities. Heat affects drying strategy. Monsoon events can complicate water intrusion. Commercial tenants may have landlord coordination issues, access limits, or tight reopening pressure.

Property owners also benefit when the contractor understands insurance-facing work standards. For a broader view of the risk and compliance side, this resource on insurance for Arizona restoration contractors is a useful reference.

When the property is damaged and income is on the line, a capable restoration partner isn't just cleaning up the mess. They're helping preserve the facts your claim may depend on.

If your Phoenix-area home or commercial property has been hit by water, fire, smoke, mold, or another sudden loss, Restore Heroes can help you take the next practical step. Their team handles emergency mitigation, detailed documentation, and communication that supports a more organized insurance process, so you can focus on getting the property and your routine back on track.