When water is pouring through a ceiling, smoke is still in the air, or mold is spreading behind drywall, most homeowners do the same thing. They grab a phone and search for help fast. In that moment, every company starts to look similar. The words licensed, bonded, and insured show up everywhere, but few people explain what those terms protect.

That confusion can get expensive.

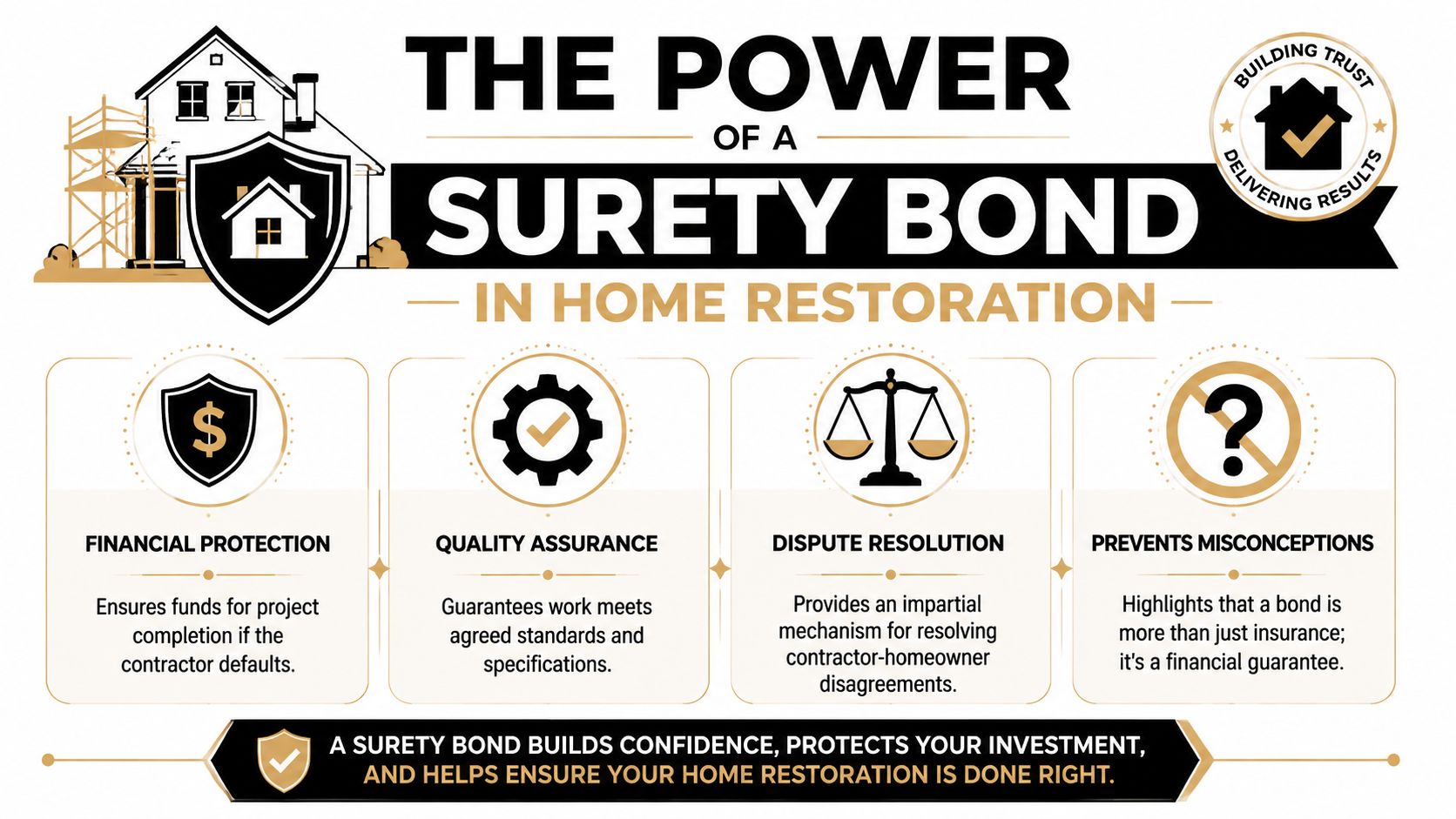

If you're hiring a bonded and insured contractor, you need to know that those are two different protections. A bond helps if a contractor fails to meet certain legal or contract obligations. Insurance helps if something goes wrong on the job, like property damage or a worker injury. And one of the biggest misunderstandings is this: a bond usually is not a promise that every part of the workmanship will be perfect.

A worried homeowner doesn't need jargon. You need a clear way to judge risk, ask better questions, and avoid false confidence when your house already feels upside down.

Your First Call After a Home Disaster

The first hours after a disaster are messy. You're trying to stop more damage, protect your family, talk to your insurer, and find a company that can show up now. That pressure makes it easy to hire the first contractor who sounds available.

Speed matters. So does knowing what you're agreeing to. If you need 24/7 emergency restoration response, ask about credentials before crews unload equipment.

Why these words matter under stress

“Bonded and insured” isn't decoration on a website. Those words point to two separate financial protections.

One matters if the contractor doesn't carry out certain obligations tied to the job or license. The other matters if the work itself causes damage or someone gets hurt on your property. If you mix them up, you may think you're protected when you're not.

Practical rule: Before you sign anything, ask the contractor to explain in plain English what their bond covers and what their insurance covers. If they can't answer clearly, keep looking.

What homeowners usually miss

A homeowner in crisis often asks, “Are you insured?” That's a good start, but it isn't enough. You should also ask whether the company is bonded, what type of bond they carry, and whether the bond relates to licensing, payment, or job performance.

The bigger issue is assumption. Many people hear “bonded” and think it means “my house is protected from any bad work.” That isn't how bonds usually work. A bond can be important. It just doesn't replace insurance, and it doesn't replace careful vetting.

That's why these terms deserve a closer look before a crew starts tearing out drywall, setting drying equipment, or packing out your belongings.

Decoding Bonded vs Insured for Homeowners

The easiest way to understand this is to think of a bond and an insurance policy as two different tools.

A bond is a financial guarantee tied to obligations. A policy is protection against covered losses. They may sit next to each other in a contractor's paperwork, but they don't do the same job.

What bonded means

A contractor bond is a three-party agreement. The contractor is the principal. The customer or public authority being protected is the obligee. The surety company backs the bond.

If the contractor fails to fulfill certain duties and a valid claim is paid, the surety can pay up to the bond limit. But the contractor has to repay the surety. That's the key difference. The risk doesn't disappear. It stays with the contractor.

That structure is why many people describe bonding as closer to a credit guarantee than a normal insurance policy. CCIS Bonds explains that the principal remains legally obligated to repay the surety for losses, costs, and fees after a claim is paid.

What insured means

Insurance is more familiar. It's usually a two-party arrangement between the contractor and the insurer. If there's a covered claim, the insurer handles the loss under the policy terms.

For homeowners, the two insurance types that matter most on a restoration job are:

- General liability insurance protects against certain accidental property damage or third-party injury connected to the work.

- Workers' compensation insurance helps cover employee injuries that happen on the job.

If a technician damages part of your home while moving equipment, or an employee gets injured while working in a wet structure, insurance is the protection you're looking for, not the bond.

Bonded vs. Insured at a Glance

| Aspect | Bonded Contractor | Insured Contractor |

|---|---|---|

| Main purpose | Guarantees certain legal and contractual obligations | Covers certain accidental losses and liability |

| Who is protected | The obligee, often the project owner or licensing authority | The contractor and covered third parties, depending on the policy |

| What may trigger a claim | Failure to fulfill bond-backed duties, such as completion or payment obligations | Covered accidents, property damage, or injuries |

| Who pays first | The surety may pay a valid claim | The insurer may pay a covered claim |

| Who ultimately carries the risk | The contractor must reimburse the surety | The insurer absorbs covered risk under the policy terms |

| Best way to think about it | A financial guarantee tied to compliance or performance | A safety net for accidents and liability |

The clearest distinction

One of the best plain-language summaries comes from Surety Bonds Direct's explanation of licensed, bonded, and insured contractors. It explains that bonded status covers legal and contractual obligations, such as paying unpaid subcontractors or arranging completion if a contractor fails to finish. It also explains that insurance protects against on-site injuries or property damage. Most important, it notes that insurance transfers risk to the insurer, while a bond keeps the ultimate risk with the contractor, who must indemnify the surety for paid claims.

A bond protects the obligation. Insurance protects against accidents.

That one sentence will help you sort out most of the confusion.

Where homeowners get tripped up

People often ask one question when they really need to ask three:

- Are you licensed?

- Are you bonded?

- Are you insured?

Each answer should come with paperwork. A verbal “yes” isn't enough when your home and finances are on the line.

Why a Bonded Contractor is Crucial for Restoration Work

Restoration projects can move fast and still be financially complicated. Drying, demolition, debris removal, specialty cleaning, subcontractors, and rebuild work can overlap. If a contractor walks off the job or collapses halfway through, the mess isn't only physical. It's legal and financial.

That's where bonding matters most.

A bond helps when the job falls apart

A surety bond is important because it creates a path for financial recourse if the contractor fails in a way the bond covers. In practical terms, that can mean funds are available to address unfinished obligations, such as bringing in another contractor or dealing with unpaid project participants, depending on the bond terms.

That matters more than many homeowners realize. A 2023 economic analysis reported in Construction Executive found that unbonded construction projects where a contractor defaults incur a cost of completion 85% higher than projects protected by surety bonds. The same source says 68% of homeowners in major US markets incorrectly assume a bond covers workmanship defects, which can leave them exposed when a claim is denied.

If you want a plain overview of the job itself, this guide on what a restoration company does helps show how many moving parts can exist on a loss.

The myth that causes trouble

Here is the costly myth: a bond does not automatically mean the bond covers bad workmanship.

Many homeowners often get blindsided. They hear “bonded” and assume, “If the work is sloppy, the bond will pay to fix it.” Sometimes a separate warranty, contract term, maintenance bond, insurance policy, or licensing complaint process may apply. But bonded status by itself should not be treated as a blanket quality guarantee.

If you're hiring after water or fire damage, treat a bond as a completion and compliance backstop, not a universal quality promise.

That distinction changes how you interview contractors. You don't stop at “Are you bonded?” You ask for a written scope, material details, drying documentation, cleanup standards, and insurance proof. Bonding is one layer. It isn't the whole shield.

Why this matters more in restoration than routine remodeling

Restoration work happens in damaged buildings. Moisture can migrate. Smoke residue can spread. Contents may need pack-out and cleaning. Temporary repairs may happen before permanent rebuild work starts. Because the job is urgent, homeowners sometimes skip normal vetting steps.

That's exactly when you should slow down enough to verify the bond.

A bonded contractor doesn't guarantee a perfect experience. But when the project is already high stress, a bond reduces one major risk. It gives you a formal financial mechanism if the contractor fails to meet the obligations the bond is designed to support.

The Role of Insurance in Protecting Your Property and Wallet

Insurance becomes real when you picture the job inside your house.

A crew arrives after a flood. Hoses run through hallways. Air movers and dehumidifiers get set in place. Baseboards come off. Cabinets may be detached. Containment barriers go up. People are carrying tools and equipment through rooms that may already be wet, smoky, unstable, or contaminated.

The property damage scenario

Let's say a technician moves drying equipment into a bedroom and gouges hardwood flooring. Or a containment pole slips and cracks a light fixture. That's not a bond issue. That's the kind of situation where general liability insurance may matter.

Insurance can also matter if a contractor's actions cause additional damage while trying to mitigate the original loss. If a homeowner assumes the bond covers that kind of accident, they may be looking in the wrong place when it's time to file a claim.

The worker injury scenario

Now consider a different problem. A worker slips on a wet tile floor in your kitchen and gets injured while setting up extraction equipment. If that contractor doesn't carry proper workers' compensation coverage, the financial and legal situation can get ugly fast.

You don't need to become an insurance expert. You do need to know enough to ask for proof. If you want a basic outside reference for what these protections often look like, Select Insurance Group has a useful overview of customized policies for contractors.

Ask for current certificates, not promises. Coverage only helps if it's active when the loss happens.

What to review before work starts

Ask the contractor for a Certificate of Insurance and read it carefully. You don't need to decode every line. Focus on a few basics:

- Named insured should match the company you're hiring.

- Effective dates should show the policy is current.

- Coverage types should include liability and, where appropriate, workers' compensation.

- Carrier information should be listed clearly so you can verify it.

Homeowners also benefit from understanding how their own policy may interact with contractor-caused loss. This guide on how to read a homeowners insurance policy can help you spot where your insurer's responsibilities begin and end.

Insurance is the accident shield

If bonding answers, “Will the contractor meet certain obligations?” insurance answers, “What happens if someone gets hurt or property gets damaged during the work?”

That's why a bonded and insured contractor matters. The bond and the policy protect against different kinds of risk, and a homeowner needs both in play.

How to Verify a Contractor is Bonded and Insured in Arizona

Verification doesn't have to be complicated. You can do most of it in a short sitting at your kitchen table.

For many contractor licenses in states like Arizona, a Corporate Surety Bond is a mandatory licensing requirement. The bond must name the individual license holder and be payable directly to the licensing board, creating a financial guarantee that the contractor will follow state laws and industry standards, as described in the Oklahoma CIB contractor requirements reference used here for bond structure and licensing context.

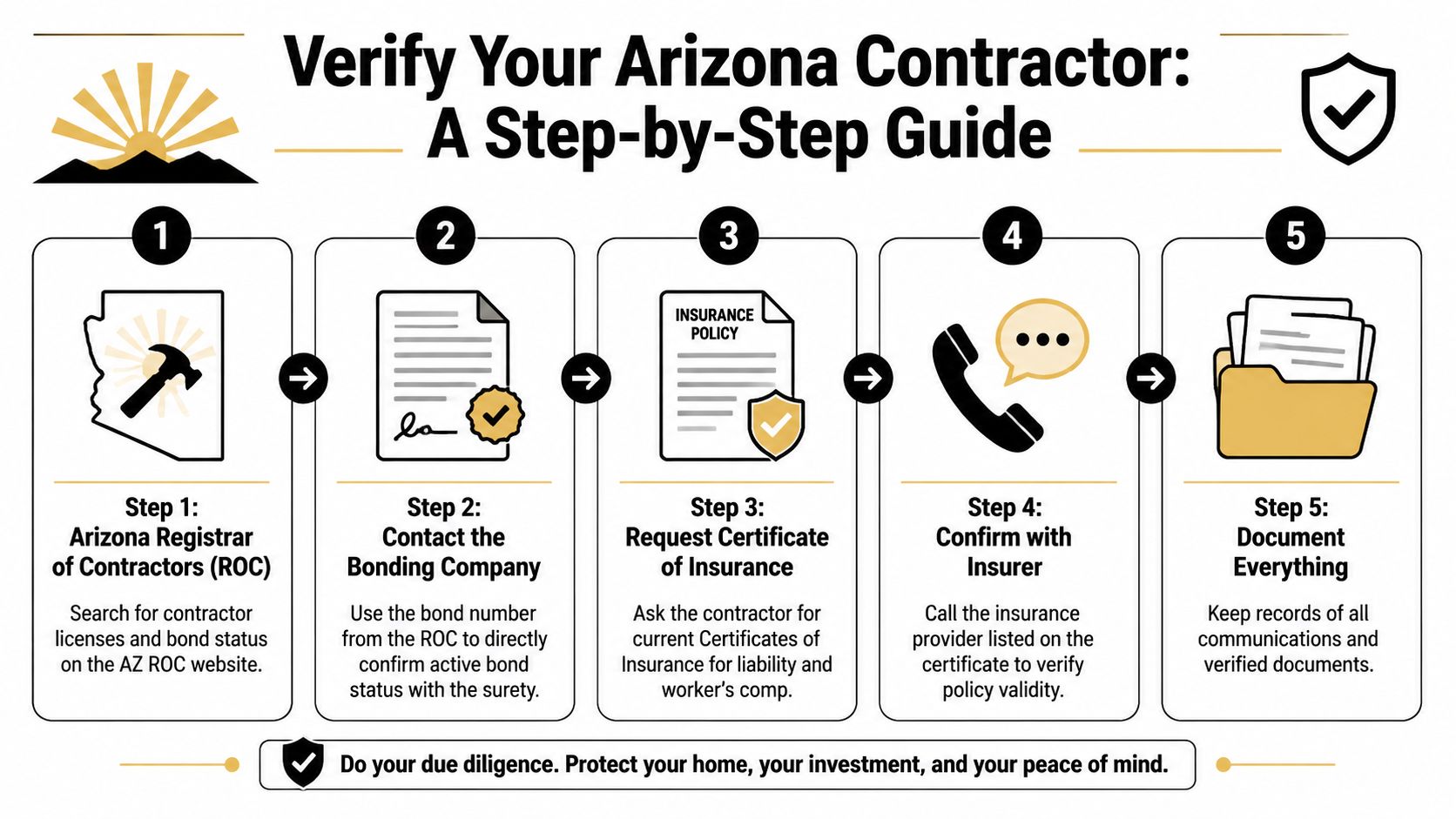

Start with the Arizona license record

Ask for the contractor's full legal business name and license number. Then search the Arizona Registrar of Contractors record. You're looking for the basics first: active license status, correct classification, and whether the listed company matches the paperwork you were given.

This is also where you can begin spotting mismatch problems. If a proposal says one company name but the license belongs to another entity, stop and ask why.

One Arizona option homeowners may encounter during this search process is Restore Heroes' flood restoration services, which are tied to the company's licensing and service information. Whatever company you review, the name on the proposal, license, bond, and insurance documents should line up.

Confirm the bond directly

Don't stop at “bonded” on a business card. Ask for:

- Bond number

- Name of surety company

- Type of bond

- Name of bonded principal

Then call the surety or use its verification channel if available. Ask whether the bond is active and whether the bonded principal matches the contractor you're considering.

Homeowner check: If the bond names a different person or entity than the one on your contract, ask for clarification before work begins.

Review the insurance certificate carefully

A Certificate of Insurance isn't the policy itself, but it's the standard summary document contractors use to show current coverage.

Check these items:

Business name

It should match the company on your contract.Current dates

Expired coverage doesn't help you.Coverage listed

Look for liability coverage and workers' compensation where applicable.Insurance carrier contact information

Use it to verify the certificate directly.

A contractor should expect this request. You're not being difficult. You're protecting your home.

Here is a quick video that helps explain contractor verification in a practical way:

Keep a paper trail

Save screenshots, email confirmations, certificates, and the final contract. If anything changes during the job, ask for updated paperwork. That includes policy renewals, subcontractor involvement, or a revised project scope.

A careful file won't stop a bad job by itself. But it gives you an advantage, clarity, and a record if questions come up later.

Your Hiring Checklist for Arizona Restoration Contractors

By the time you're comparing bids, the goal isn't to find the contractor with the smoothest sales pitch. It's to find the one whose credentials, paperwork, and answers hold up under stress.

That matters in Arizona because bonding isn't a fringe requirement reserved for giant commercial jobs. On the high-stakes end of the market, bonding is standard. Federally funded projects, including CHIPS Act semiconductor facilities, require bonding under the Miller Act for contracts exceeding $150,000, and public construction spending topped $521 billion in late 2025, showing how central bonding is to serious construction work, according to this Willis Towers Watson reporting summarized by Grit Insurance.

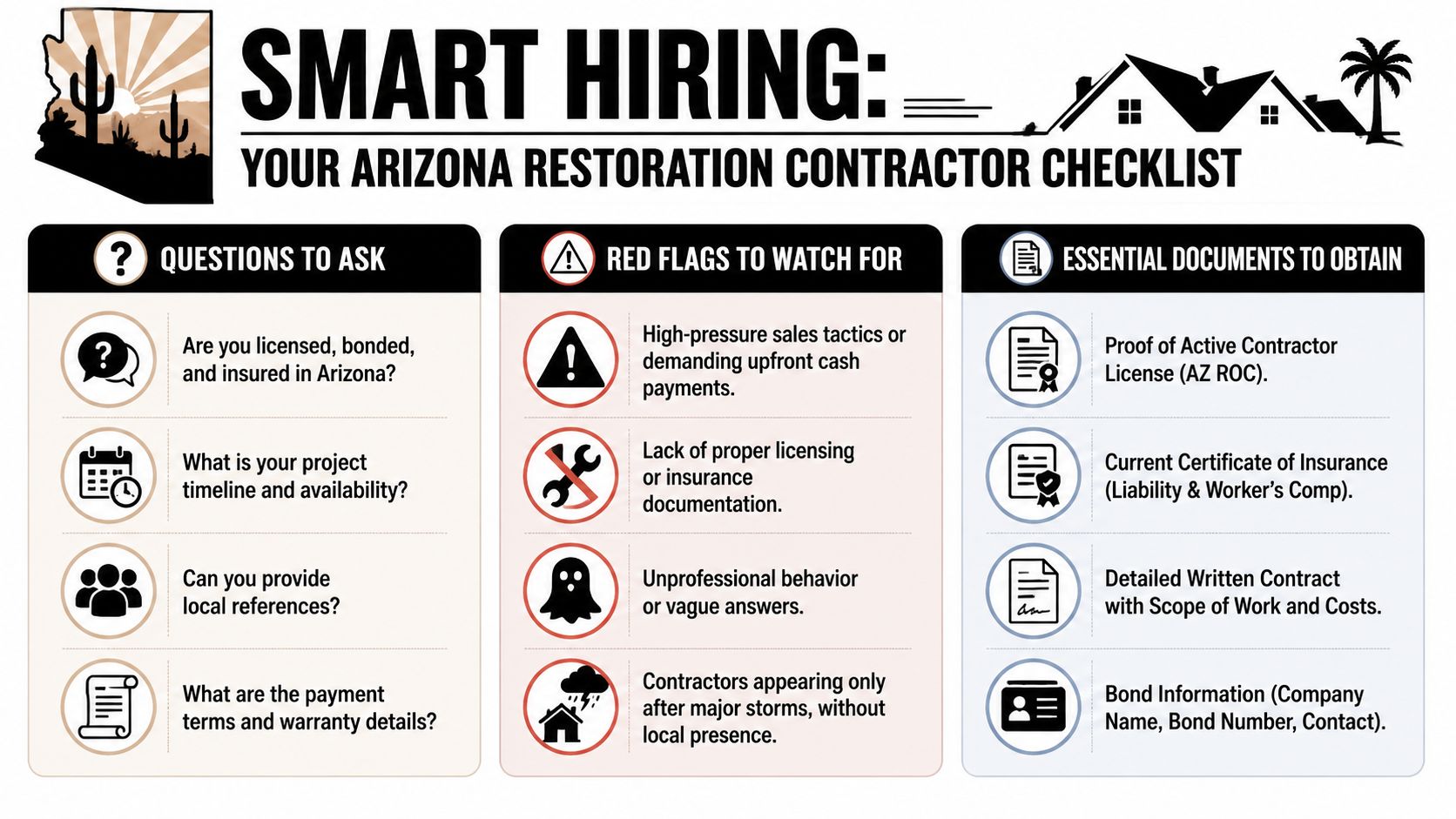

Questions to ask

Bring these into every estimate meeting.

Ask about licensing first

“What is your Arizona license number, and which company name does it appear under?”Ask for bond details second

“What type of bond do you carry, and what is the surety company's name?”Ask for insurance documents, not verbal assurances

“Can you send a current certificate of liability insurance and workers' compensation coverage?”Ask about restoration-specific qualifications

“Do your technicians follow IICRC standards for water, fire, or mold work?”Ask about insurance claim coordination

“How do you document damage, drying, demolition, and communication for the adjuster?”Ask how the company communicates during the job

“Who updates me, how often, and what happens if the scope changes?”

Red flags to spot

Some warning signs show up before work even begins.

Pressure to sign immediately

A homeowner dealing with a disaster is vulnerable. A contractor who pushes for a rushed signature without clear paperwork is increasing your risk.Requests for large cash payments upfront

A clear payment schedule in writing is safer than vague cash demands.Fuzzy answers about bond or insurance status

If the salesperson says, “We have all that,” but won't provide documents, treat that as a problem.Storm-only presence

Be careful with companies that appear right after severe weather but don't show a stable local footprint.

Final vetting steps

Before you sign, run this short final check:

Match every name

The contractor name on the estimate, license, bond, and insurance certificate should match.Read the written scope

Make sure demolition, drying, cleaning, pack-out, and rebuild responsibilities are spelled out.Get local references

Speak to people who had similar losses, not just general remodeling work.Review the payment terms

Understand when payments are due and what documentation supports them.Confirm service category fit

A company that handles kitchen remodels isn't automatically equipped for emergency mitigation. If you're comparing providers for a water loss, review a contractor that specifically performs water damage restoration work.

Choose the contractor who can prove their credentials calmly and clearly. In restoration, paperwork is part of the cleanup.

A bonded and insured contractor gives you a stronger starting point, but the safest hiring decision comes from verification, written scope control, and realistic expectations about what each protection does.

If you need help reviewing restoration credentials after a water, fire, mold, or biohazard loss, Restore Heroes is one Arizona company homeowners can consider. The company states that it is licensed, bonded, insured, and IICRC-certified, and homeowners can ask for the same license, bond, and insurance documentation discussed above before deciding whether it's the right fit for their property.